The Transcript 1Q25 Letter

Reviewing the key themes from 1Q25 through C-suite quotes

Summary: The first quarter is ending. Here are some themes that we’ve noticed in transcripts throughout the last few months.

Editor’s Note: We have made this edition available to all subscribers. If you’re not a premium subscriber already, we hope that you will read this and subscribe!

Macro

Markets began the year with a high level of optimism about the economy and specifically about the incoming administration. The consensus was that the Trump administration would help re-kindle animal spirits. But in the last few weeks that narrative has hit turbulence thanks in part to the administration itself. The second Trump administration has brought volatile policy change, and markets are watching these shifts with concern.

"Overall, the U.S. economy starts the year in good shape" – Federal Reserve Governor Lisa Cook [13th Jan - A Good Start to 2025]

"2025 is off to a great start" – Delta Air Lines CEO Ed Bastian [13th Jan - A Good Start to 2025]

Markets are struggling to digest rapid news flow and trying to handicap whether actions taken by the administration will lead to long term shifts in America’s leadership of the global economy. The administration’s actions challenge pillars of the post World War II order, including even deference to legal precedent in the United States.

"We looked at, for example, the last 15 large sell-offs in the last 15 years in the U.S., this is the one with the highest level of dispersion, i.e. the lowest correlation...you have Alibaba, up 74% and yet NVIDIA I think in one day had the largest market cap down move. This is all this year” — Morgan Stanley (MS 0.00%↑) Co-President Dan Simkowitz [24th Mar - Unusual Uncertainty]

"The level of uncertainty is a little bit higher, and that has kept some things on the sidelines. The more we can have certainty on the policy agenda as we move forward, the better that’s going to support capital investment and growth." — Goldman Sachs (GS 0.00%↑) CEO David Solomon [17th Mar - Encountering Turbulence]

Most importantly though the changes that the administration is making are being done in a relatively erratic way. Tariffs are announced one day and rescinded the next. When capital markets are faced with this type of volatile change, it makes it hard to discount the future and so capital tends to get spooked.

"Everybody’s paralyzed...What decision do you make? Do you want to go left or right? Are we going to grow the business? Well, I don’t know. Are there tariffs or not?" – ON Semiconductor (ON 0.00%↑) CEO Hassane El-Khoury [3rd Mar - Paralysis]

“Our customers really haven't moved off where they were in November and all honesty, which is the wait and see” - First Horizon (FHN 0.00%↑) CFO Hope Dmuchowski [10th Mar - Volatile Policy, Volatile Markets]

The Fed is not positioning itself to give any cover to the administration. Powell is shielding the Fed behind its dual mandate of price stability and full employment. In doing so, he is taking a literalist approach to the current environment. Powell’s view is that tariffs may be inflationary and so the Fed is on hold in order to fight their potentially inflationary effects.

"It can be the case that it's appropriate sometimes to look through inflation if it's going to go away quickly without action by us, if it's transitory. And that can be the case in the case of tariff inflation... So, I think, I think that's kind of the base case." — Federal Reserve Chair Jerome Powell [24th Mar - Unusual Uncertainty]

While academically convenient, this argument obfuscates a significantly more important silent battle that Powell is currently fighting. Powell is struggling to maintain the Fed’s independence, yet he is also putting the Fed in between the administration and its policy objectives. He is therefore tip-toeing the Fed closer to the administration’s cross hairs.

"We do not need to be in a hurry, and are well positioned to wait for greater clarity...The costs of being cautious are very, very low. The economy is fine. It doesn't need us to do anything really. We can wait, and we should wait." — Federal Reserve Chair Jerome Powell [10th Mar - Volatile Policy, Volatile Markets]

We take the Fed to be independent today; however the independence of the Fed is not constitutionally mandated and has never been legally challenged. Suffice it to say that both sides are playing with fire.

International

Along with the volatile nature of US policy, it has become more fashionable for capital to flow overseas. The Trump administration has somewhat inadvertently lit a spark under the international economy by forcing trading partners to focus more internally and beyond the existing system of American leadership of the global economy.

"There is a strong willingness in Europe to spend much more, much more and much more. Now the proof is in the pudding where the contracts will come, we will be ready, but it's no use to be ready too much in advance." — Thales (THLEF) CEO Patrice Caine [10th Mar - Volatile Policy, Volatile Markets]

European stocks were already trading at low multiples and so the surge of energy is perhaps as much a rebalancing of valuations against low multiples as any indication of a true change in fundamentals. Still, things do appear to be changing, especially given that European countries are being forced to assess their own competitive practices and historically more anti-competitive leanings.

"There is increased discussion within the European Union regarding creating and protecting an attractive environment for capital to be invested in industrial activities." — Commercial Metals (CMC 0.00%↑) CEO Peter Matt [24th Mar - Unusual Uncertainty]

Technology

Along with broader volatility, the market’s hottest trend–AI–has become marginally less fashionable in the first quarter. NVIDIA has been a laggard and so has the NASDAQ. The narrative is that this is partially due to the success of Deep Seek at meeting performance of leading LLMs with less computing cost. But it’s more likely that the underperformance has been the result of a high beta pull through of the macro volatility noted above.

“To see the DeepSeek new model, it’s super impressive in terms of both how they have really effectively done an open-source model that does this inference-time compute, and is super-compute efficient” - Microsoft (MSFT 0.00%↑) CEO Satya Nadella [27th Jan - The Golden Age]

“We are aware of the recent revelations of DeepSeek and the implications that it portends a diminished demand for advanced semiconductors in support of the AI infrastructure build-out" — KLA (KLAC 0.00%↑) CEO Richard Wallace [3rd Feb - The Wind of Optimism]

At this time the momentum in AI appears unstoppable and nothing has truly changed about the fundamentals of infrastructure requirements to deliver and expand AI’s reach into the economy. If an AI model is more efficient it just means that it can do more with less compute and even more with more compute. At this time industry’s appetite for “compute” is basically insatiable and truly only limited by energy access.

“Jevons paradox strikes again! As AI gets more efficient and accessible, we will see its use skyrocket, turning it into a commodity we just can't get enough of.” - Microsoft (MSFT 0.00%↑) CEO Satya Nadella [27th Jan - The Golden Age]

…our own experience supports the theory that increased compute efficiency enables more adoption of AI in our platforms. The demand is clearly elastic." — KLA (KLAC 0.00%↑) CEO Richard Wallace [3rd Feb - The Wind of Optimism]

"This last year, this is where almost the entire world got it wrong: the computation requirement…The amount of computation we need, at this point, as a result of Gentex AI and reasoning, is easily 100 times more than we thought we would need at this time last year." — Nvidia (NVDA 0.00%↑) CEO Jensen Huang [24th Mar - Unusual Uncertainty]

“Compute is still very much a critical part of the infrastructure needed for AI—not only for accessibility but also for exploring new ideas. If you're innovating at the frontier, you have to experiment at scale...we probably need more compute than ever." - Alphabet (GOOGL 0.00%↑) Google DeepMind CEO Demis Hassabis [18th Feb - Nobel Prize Winning Kids]

Consumer

Lost in the shuffle of these major economic forces is the former powerhouse of capital markets, the American consumer. Large segments of American consumers are hurting financially and experiencing what would be an obvious and growing recession in any other era.

"It's definitely been a slow start to the year…all of us are watching consumer confidence and, ultimately, are we seeing potential for slower levels of demand…" — Stanley Black & Decker (SWK 0.00%↑) CEO Don Allan [10th Mar - Volatile Policy, Volatile Markets]

“I'm still nervous about the lower-end consumer” - — Simon Property Group (SPG 0.00%↑) CEO David E. Simon [11th Feb - The AI Arms Race]

"...clearly, the lower-income consumers are more impacted” - Nestlé (NESN) CEO Laurent Freixe [18th Feb - Nobel Prize Winning Kids]

Our consumer remains under pressure from accumulated inflation and higher interest rates..." — Walgreens Boots Alliance (WBA 0.00%↑) CEO Tim Wentworth [21st Jan - Too Good?]

High income consumers have been able to continue to carry the economic load; however, there are signs that even this segment is feeling overstretched. Income growth is lagging inflation for a significant percentage of the population and only a small percentage of consumers have meaningful direct exposure to capital markets. These dynamics could become worse over time as AI disintermediates larger portions of the knowledge economy.

"Higher income consumers, we define as over $100,000 household income. We continue to see that trade down and retention of those customers." — Ollie's Bargain Outlet (OLLI 0.00%↑) COO Eric van der Valk [24th Mar - Unusual Uncertainty]

"What has really become apparent leaving Q4 and moving into Q1 is the trade-down is back, both the mid and upper end trade-down, and as we moved into Q4, seems to be accelerating… I would tell you nothing that we've seen so far would show that that trade-down has slowed down. If anything, we may have seen it accelerate a little bit in the last few weeks." — Dollar General (DG 0.00%↑) CEO Todd Vasos [17th Mar - Encountering Turbulence]

"We're seeing higher engagement across income cohorts, with upper-income households continuing to account for the majority of share gains." – Walmart (WMT 0.00%↑) CFO John Rainey [24th Feb - Forever Blossom]

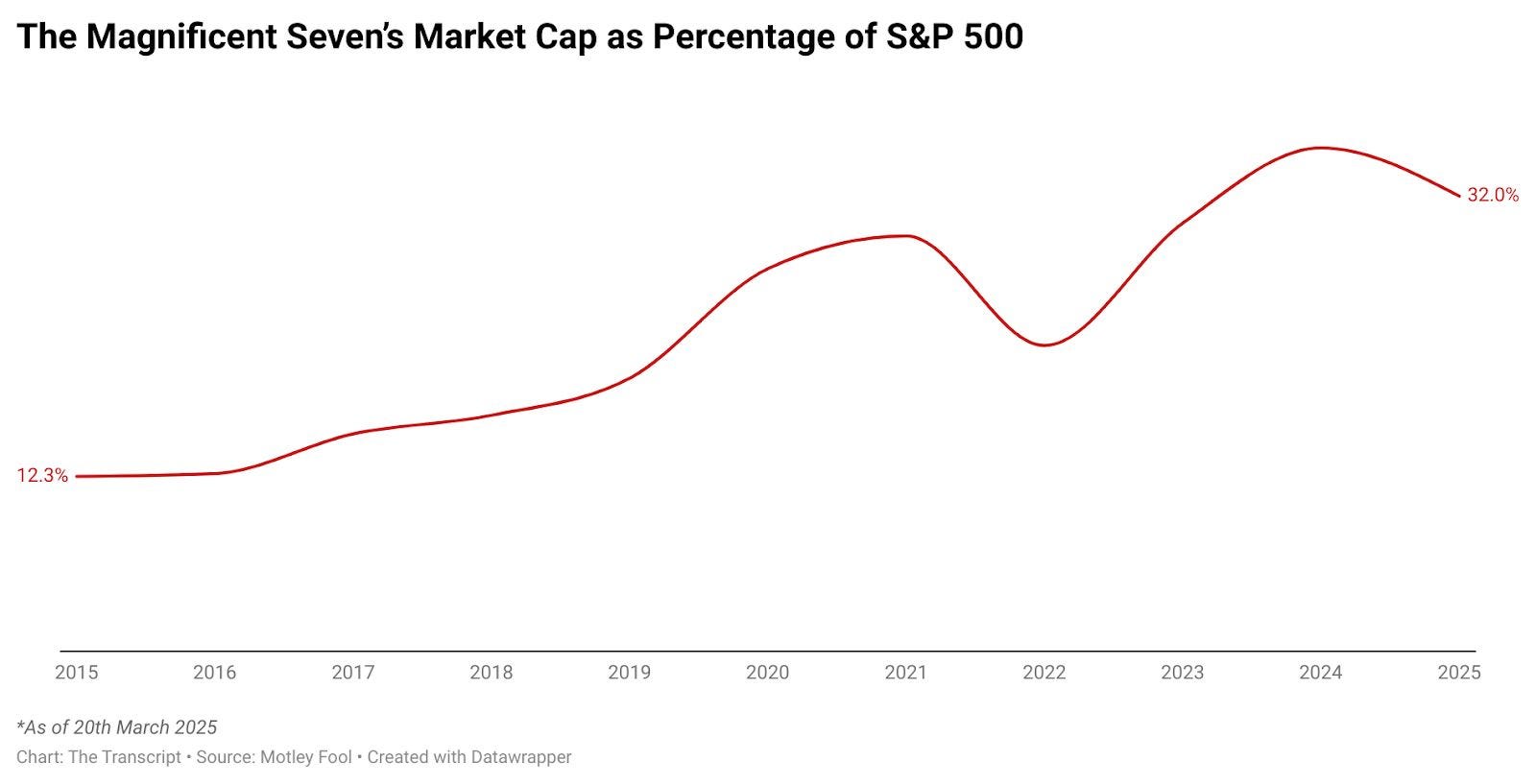

The consumer has become mathematically less relevant to capital markets though–the Magnificent 7 tech stocks represent >30% of the S&P 500.

Looking forward

The course of US capital markets for the rest of 2025 would seem to depend on the market’s level of comfort with the Trump administration’s policies. For now the pressure of global capital markets is beginning to bear down on the Trump administration, and Trump is doing what he knows how to do best–doubling down. This could cause a spiral of consternation for capital markets, especially when administration officials seem to wave aside concerns about a recession.

"The market and the economy have become hooked, become addicted, to excessive government spending, and there’s going to be a detox period...Could we be seeing this economy that we inherited starting to roll a bit? Sure. Look, there’s going to be a natural adjustment as we move away from public spending." — US Treasury Secretary Scott Bessent [10th Mar - Volatile Policy, Volatile Markets]

A contrarian view though is that Trump will actually “win” his trade war and American capital markets will come out on top. This seems somewhat improbable and yet so did Trump winning a second (let alone a first) term as President. Trump displays unparalleled anti-fragility, which may end up carrying the day on otherwise puzzling policy decisions.

"If we tear the world apart—I call it the economic battlefield—in trade, pricing, you know, us against Europe, us against China—yeah, we're going to have an issue. So, you know, America First is fine. America alone—if we end up alone because, you know, we're tearing the world asunder—we will have made a mistake." — JPMorgan (JPM 0.00%↑) CEO Jamie Dimon [10th Mar - Volatile Policy, Volatile Markets]

If the Trump administration does lose the fight it’s picking it would be catastrophic for US capital markets and the rails of international finance in general. The global financial network seems too deeply intertwined and tightly knit to disintegrate from its current form though. Therefore, the odds are in favor of continued flow of power and capital to the United States.

Looks like Powell's walkin' a tightrope between independence and the admin's goals. It's a wild game of balancing act, and the stakes couldn't be higher. The Fed's gotta keep its focus sharp while the rest of the world shakes things up. Curious to see how this plays out!

Hello there,

Huge Respect for your work!

New here. No huge reader base Yet.

But the work has waited long to be spoken.

Its truths have roots older than this platform.

My Sub-stack Purpose

To seed, build, and nurture timeless, intangible human capitals — such as resilience, trust, truth, evolution, fulfilment, quality, peace, patience, discipline, relationships and conviction — in order to elevate human judgment, deepen relationships, and restore sacred trusteeship and stewardship of long-term firm value across generations.

A refreshing take on our business world and capitalism.

A reflection on why today’s capital architectures—PE, VC, Hedge funds, SPAC, Alt funds, Rollups—mostly fail to build and nuture what time can trust.

“Built to Be Left.”

A quiet anatomy of extraction, abandonment, and the collapse of stewardship.

"Principal-Agent Risk is not a flaw in the system.

It is the system’s operating principle”

Experience first. Return if it speaks to you.

- The Silent Treasury

https://tinyurl.com/48m97w5e