Episode Summary: In this episode, we discuss the strong start to the Q3 earnings season last week as the big banks reported.

The episode is based on yesterdays’ newsletter which is available below:

The free version of the newsletter is available here. A transcript of this podcast, with relevant images and quotes, is available, for subscribers only, after the show notes below. Subscribe to access it:

Show Notes:

00:00:00 Introduction

00:00:17 Strong GDP growth despite inflation

00:01:54 Supply chain issues have dwarfed demand recovery

00:03:25 Inflation hitting small businesses disproportionately

00:07:34 Surge in energy prices

00:08:19 Tightness in the labor market persists

00:10:03 Squid Game global euphoria

00:12:59 Banks loosening credit in commercial real estate

Episode Transcript:

Introduction

Scott: [00:00:00] Welcome everyone to a new episode of The Transcript podcast. You've got me, Scott Krisiloff, I'm the editor of The Transcript, along with Erick Mokaya who's our lead author. We send out a new version of The Transcript newsletter earlier this week, and it was the beginning of earning season last week.

Strong GDP growth despite inflation

So the banks were reporting. Got good insight into what the banks are seeing in the economy. They continue to see a strong driven by really strong consumer spending. Bank of America talked about consumer spending in payments up 23% over 2019, just really strong growth along with some comments about GDP growth in the 5.5 to 6% range, which again, is really really large, especially when you consider that’s real GDP that people are quoting and not nominal GDP, where we have another five, 5% plus inflation on top of that.

Speaking of inflation, inflation was again, a very prominent topic in conference calls last week. The thing that stood out most was actually a presentation from Fed president Raphael Bostic of Atlanta who was talking about transitory is a dirty word at the Atlanta fed. Now talking about this being episodic inflation and talking about how this episode of inflation may not even be brief. Everyone's inflation expectations are getting higher even longer out and it's definitely something that the Fed is going to have to act against. Erick, any thoughts?

[00:01:31] Mokaya: I agree. The frustrating bit was about the word transitory being a swear word now at the Federal Reserve, I think they don't like the word anymore. And again, the common issues that people have is supply chain issues and inflation. Those are the topics that all the CEOs that we read about last week mostly are concerned about.

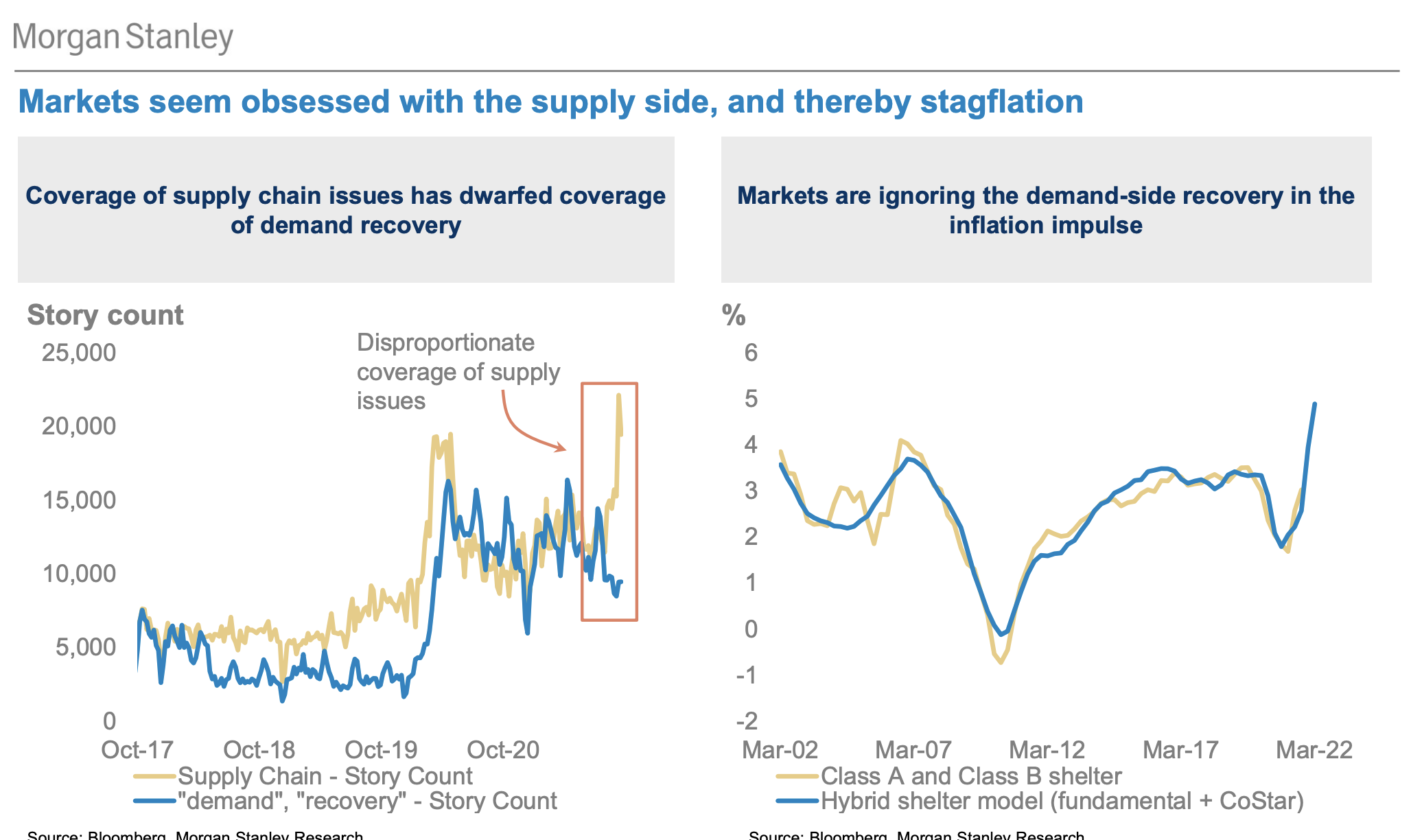

Supply chain issues have dwarfed demand recovery

But one thing that I also saw, I looked at a note from Morgan Stanley this week and that's where I wanted to ask you a question. They seem to think that the coverage of supply chain issues has actually dwarfed the coverage of demand recovery. We can see those two in play last week that there's a lot of recovery that is going on, as you say, around 6% growth, there’s projection for 2021. But then again, on the other hand, what we've been hearing constantly is about the supply chain issues. Do you think, we are a bit overblowing the issues along supply chain even though it's more an issue of demand that is way higher than the supply that we have currently?

[00:02:31] Scott: Yeah. I mean, I think you and I have done a pretty good job of covering the demand boom for the last year. And that was a theme of everything in the summer for us. It was just like the euphoric demand recovery in the US and global economy. I think demand is still really strong. I don't think that's the story anymore. Personally the story and what we keep covering is the persistence of the supply chain problems that don't seem to be getting better and may last into and through 2022. Those are drivers of inflation, but I think that there's other drivers of inflation here.

At one point in history, we used to talk about inflation being a monetary phenomenon. It's kind of crazy to me that the Federal Reserve, which is probably driving inflation by printing hundreds of billions of dollars a month, seems to advocate any responsibility in the inflationary boom that we're seeing.

Inflation hitting small businesses disproportionately

"Many companies are making healthy profits and our research team expects another strong quarter of profits by American businesses." - Bank of America (BAC) CEO Brian Moynihan

[00:03:25] Mokaya: I think, especially for the Fed, they're blaming the supply chain and they are not at all taking responsibility themselves, but something from Bank of America CEO that he said also, companies are actually making healthy profits. It's either companies have very strong pricing power most of the companies out there. They expect another very strong quarter in terms of profits from American businesses. Any thoughts on that?

“We do hear a lot about supply chain issues from that customer segment [small business]" - JPMorgan CEO Jamie Dimon

[00:03:49] Scott: Yeah, we had a quote. I can't remember if it's in this week or weeks earlier that the inflation and supply chain challenges are hitting small businesses, disproportionately, and again, Bank of America, Goldman Sachs that upper echelon, upper-tier banks are really dealing with upper-tier Fortune 100 type clients who have pricing power to be able to avoid inflation and cram inflation down on customers and suppliers. Also, have the ability to take a disproportionate share of supply chains. So, those sorts of investment banks don't necessarily see the same picture small businesses and small consumers are seeing from an inflationary standpoint where those entities are bearing the brunt of the inflation. $5, $6 gasoline is a real tax on somebody who is making minimum wage.

[00:04:45] Mokaya: Yeah, definitely. I think the smaller retailers and small businesses are the ones that are going to be disproportionately affected by this. They don't have the pricing power, they don't have the power to pass on this kind of price increases to their customers.

“I think those retailers who have big presence from a supply chain perspective and have big volumes are advantaged to be able to secure capacity and actually help mitigate and manage the cost increases that are happening in the space…If you're a small player in the marketplace, you're seeing probably greater cost increases and probably struggling to get capacity into the U.S" - Lowe's (LOW) CFO Dave Denton

But something else we talked about is what if, and I think that's a really good question which was being asked by PNC financial services and Fastenal, what if the supply chain actually flips and companies are actually stocking up a bit too much inventory right now, because right now what's happening is that a lot of stocking in terms of inventory, most of the companies and retail companies that we’ve followed in the past couple of weeks, they are building up inventory readying for the season ahead.

But then what if something flips at some point and now companies have built the next 30 to 45 days of time into the supply, and these supply chains suddenly becomes better then companies are going to be stuck with a lot of inventory, especially those ones, which are perishable maybe a bit of a challenge. Thoughts on that? And I think you highlighted it for our premium subscribers as something to note.

"…is this something that's part of our new normal that we're going to have this kind of consternation and we need to build an extra 30 or 45 days of time into the supply chain? The risk is when that flips. And again, I don't know if it's 6 months from now or 6 years from now. When that flips, we have to be acutely aware it's happening when it's happening because right now we sell $13 million worth of inventory a day. If all of the sudden stuff comes in three weeks faster, four weeks faster, you get -- well, 13 times 20 business days in a month, that's $260 million. So you could add 100, 200, $250 million of inventory really fast. If you're not dialed in and managing and -- but it's measured in weeks, and I apologize, we don't have it at our fingertips. But a 30-45 day window wouldn't surprise me, but I just don't have the accurate number at my fingertips." - Fastenal (FAST) CEO Dan Florness

[00:05:50] Scott: Yeah. I think it is reflective of the fact that this is a very classic industrial cycle on the one hand. We saw this in the 20th century frequently, this was basically the front end of a recession in the 20th century. What would happen is you would have very strong stimulated demand and you would have a supply chain, which was primarily domestic in the middle of the 20th century that wasn't able to keep up with that demand. And you would have inflationary pressures that were working through the system and at the site of inflation, the Federal Government during the 20th century would usually respond.

So if you had 5% inflation and 4% unemployment in the 1960s, you probably would already be at like 7% interest rates here and the Fed would be aggressively tightening more and more which would flip the economy into a recession. On the other side of things, you would be over inventoried because there was a demand response to the negative side.

The difference this time around is that the Federal Reserve, at least at this point has no interest in responding to these inflationary pressures to the extent that they do is withdrawing stimulus marginally. We're still going to be printing actually like heavily stimulating the economy through the middle of next year in terms of quantitative easing, which is like an emergency response measure.

And then we're not even talking about raising interest rates until thereafter. If you're a market participant here, you're looking at the Federal Reserve not really acting to tighten until late 2023, 2024 is what their path is right now. And you've got this inflation and it just means that the most likely outcome is more inflation at this point.

Surge in energy prices

[00:07:34] Mokaya: Yeah, definitely. Then we noted this week that things like energy prices are surging a lot. Rising fuel prices are definitely also worrying, especially the airlines, which have been in a bit of recovery mode, but they really worried especially for Q4, whether they're able to handle the very high increases in terms of the prices in energy. Any thoughts on that yourself or?

[00:07:58] Scott: Yeah, I mean, I think all of it, but I don't want to be an inflation alarmist here. But people are actually talking about inflation, regular people are talking about inflation here and that qualitative data again, would have elicited a totally different response from the US government 50 years ago than it does now.

Tightness in the labor market persists

[00:08:19] Mokaya: Yeah, I agree. Again, with the housing market, something that we saw in the quotes also is that there’s still limited supply, very frothy over there.

Also staffing issues continue. Some restaurants are actually having to close. I'm not sure what you're observing where you are, but I hear a lot of companies last week had to comment about how they are handling issues to do with both the supply chain and also how they're dealing with the tightness in the labor market. I heard a lot of statistics floating around about a lot of people quitting jobs in August and September. Maybe that's what's driving -- the fact that there are fewer people to actually do transportation in trucks. We saw a quote there that said that going into the Q4 transportation issues are not going to ease up.

So a couple of things to worry about, but generally as most of the CEOs said, even though there are issues, the economy is still doing well.

[00:09:23] Scott: Yeah. I hear myself being an alarmist here and the inflation right now, securities prices are benefiting tremendously from inflation, which is, again, a difference from what it would have been in the 20th century. You would have had interest rates going up cost of capital going up which would have put a bit of a lid on equity values. And today we just have this economy where somehow the inflation is all getting captured by the corporate sector. So look, it's all a normative thing of “what is good”. But yeah, if you like securities prices rising, that's good.

Squid Game global euphoria

[00:10:03] Mokaya: Well, we will have to keep looking at the Q3 earnings this week again. Any other, anything else that captured your thoughts? Maybe one more thing that I wanted to actually highlight myself is have you watched Squid Game?

[00:10:16] Scott: I have not personally watched Squid Game, but I'm glad you brought it up. Cause I think this is one of the most important things happening right now. I think it's really important because it's showing the internationalization of content. The internet is really truly hitting this inflection point in globalization where, I mean, you're sitting in Sweden right now and I'm sitting in Los Angeles and we talk every week about stuff that's going on globally.

This is a new phenomenon that attentions are actually coalescing around certain things. I was looking at Spotify the other day and some of these songs have billions of billions of listens. The entire world moving at once is kind of a crazy thing.

[00:10:59] Mokaya: Yeah. And I think that's now you captured the sentiment quite well there. Now it's about like local content hitting internationally and hitting in such a way that Squid Game is actually going to be the best in terms of TV series ever for Netflix. Which is quite amazing. They say something around 111 million people have watched at least two minutes of the episode.

I actually did watch a few minutes of it last week, just to get a sense of what the movie is all about. It's based on a story of people, someone caught up in a debt spiral and then they have to go to these games where they compete for prize money so that they're able to get that money to actually pay off their debts.

So again, it resonates to a lot of people who may be struggling, especially because of the pandemic and all. Maybe that could be the global appeal in the TV series. But generally I say a Netflix are super pumped, and at least they are reporting earnings this week so it will be interesting to get the numbers from them on what they think about the TV series.

[00:12:02] Scott: Yeah. I mean, honestly for Netflix 10 years ago, I thought it would be a Herculean lift to get to a hundred million subscribers. And now I look at it and go, I don't see why they can't get to a billion subscribers which means that there's still upside for this stock.

[00:12:18] Mokaya: And so something that I read also, I think that their strength is actually, compared to Disney, Disney have a rich IP content. So compared to them, Netflix don't have that. So they're not bound by legacy. They can take their adventures wherever it leads for them.

Last year it took them to France and then they had one of the best hitting TV series from there. And this year it takes them to South Korea to create a whole series and now they're also selling merchandise around the TV series itself. It's pretty interesting to see how the stock itself goes. But generally again, it captures the internationalization of local content, local content capturing international audiences.

Banks loosening credit in commercial real estate

"…in CRE, we see quite a robust origination pipeline, as we've fully removed any pandemic-related credit pullbacks, and we're leaning into that and we do expect to see a little bit of net loan growth going forward." - JPMorgan Chase (JPM) CFO Jeremy Barnum

[00:12:59] Scott: One other important catalyst that I think we caught last week that I just wanted to highlight before we break, is JPMorgan talking about loosening credit standards in commercial real estate. That's something we picked up earlier too in a previous issue that commercial real estate sector had been an area where there had been the most tightness because people were wondering whether people will actually go back to offices, but banks loosening credit into that sector can be a very positive catalyst for that sector. And that is one sector that's still depressed from COVID. So there may be some investment opportunities there.

[00:13:38] Mokaya: Great. I think on that note we’ll end for this week. So thank you for joining us. See you next week on The Transcripts podcast. You can leave us your comments and send us your feedback admin@theweeklytranscript.com. So see you next week. Bye.

Thanks everyone.

Share this post