In this episode, we host Sean Stannard-Stockton, the President and Chief Investment Officer of Ensemble Capital Management, and a regular reader of our newsletter. We discuss his takeaways from the latest Q3 22 earnings from companies in their portfolio including Mastercard, Starbucks, Ferrari, Home Depot, and Netflix.

The episode is based on yesterday's newsletter which is available on Substack.

A transcript of this podcast, with relevant images and quotes, is available for all subscribers after the show notes below. Our podcast is available on Apple Podcasts, Spotify, Google Podcasts, YouTube, and Amazon Music.

Show Notes

00:00:00 Introduction

00:02:33 Why Sean enjoys the Transcript and Earnings Calls

00:05:37 Focusing on the Long Term While Engaging with Earnings

00:08:03 Macro Perspectives

00:12:58 The Ensemble Approach to Investing

00:14:32 Ferrari and Luxury

00:22:02 Mastercard and Payments

00:31:11 Netflix and Streaming

00:41:00 Home Deport and The State of Retailers

00:46:54 Concluding Thoughts

Transcript

Introduction

[00:00:00] Mokaya: Thank you so much for joining us, Sean. It's really a pleasure. We've been communicating for a while, and it's really nice to finally have you on spaces. Before I give you time to introduce yourself, I would say this is the Transcript. We spend a lot of time on earnings calls, sometimes between 50 and 100 transcripts per week just to get that timeless wisdom from management teams, we aggregate those quotes and put them in a newsletter that we send out every week. At the end of the quarter, we aggregate that into a quarterly letter. What we've been trying out on spaces and on our podcasts is to host people, spend some time on earnings calls to see what they think in terms of what they learn in the process, and share their wisdom from their perspective. We are happy to have Sean. Sean is a long-time investor and takes into consideration the earnings calls as much as he can. Sean, you can start by introducing yourself, and what you do at Ensemble Capital.

[00:00:52] Sean: Sure. My name's Sean Darren Stockton. I'm the Chief Investment Officer of Ensemble Capital. We manage about one and a half billion dollars. We're a wealth management firm that has managed its own in-house US equity strategy, US listed equity strategy coming on almost 20 years now. A wide range of clients, about a billion of our total AUM is our equity strategy, and that's both across our wealth planning clients as well as a significant number of institutional clients, family offices, direct investors, and then we have a mutual fund, the Ensemble Fund. My role as CIO is overseeing the team of analysts. I'm the lead analyst on about a third of the portfolio myself, and I'm looking forward to jumping into the details here. And quickly, just to give a plug for your service, I'm a subscriber to the Transcript, and I have this idea about investing in general, that up until the end of the 1990s, a lot of investors' job was to try and get access to information that was proprietary in some way.

And after the internet became ubiquitous more and more, our role as investors is not so much to go find information as it is to filter out the enormous firehose information we all have been exposed to. And so I feel like one of the most important things to do is create your own filters and recognize you don't want to filter out the information you don't want to see, right? But filtering out the noise and latching onto the signal. And so the reason I appreciate your service so much is that you guys clearly are able to pick out important signals from all the noise of earnings calls. And so for us, it's a really helpful piece. And for listeners, I'm just saying this off the cuff because it's true. We haven't been paid to say it or anything like that it's just it's a great service and I'm really excited to be on the call here.

Why Sean enjoys the Transcript and Earnings Calls

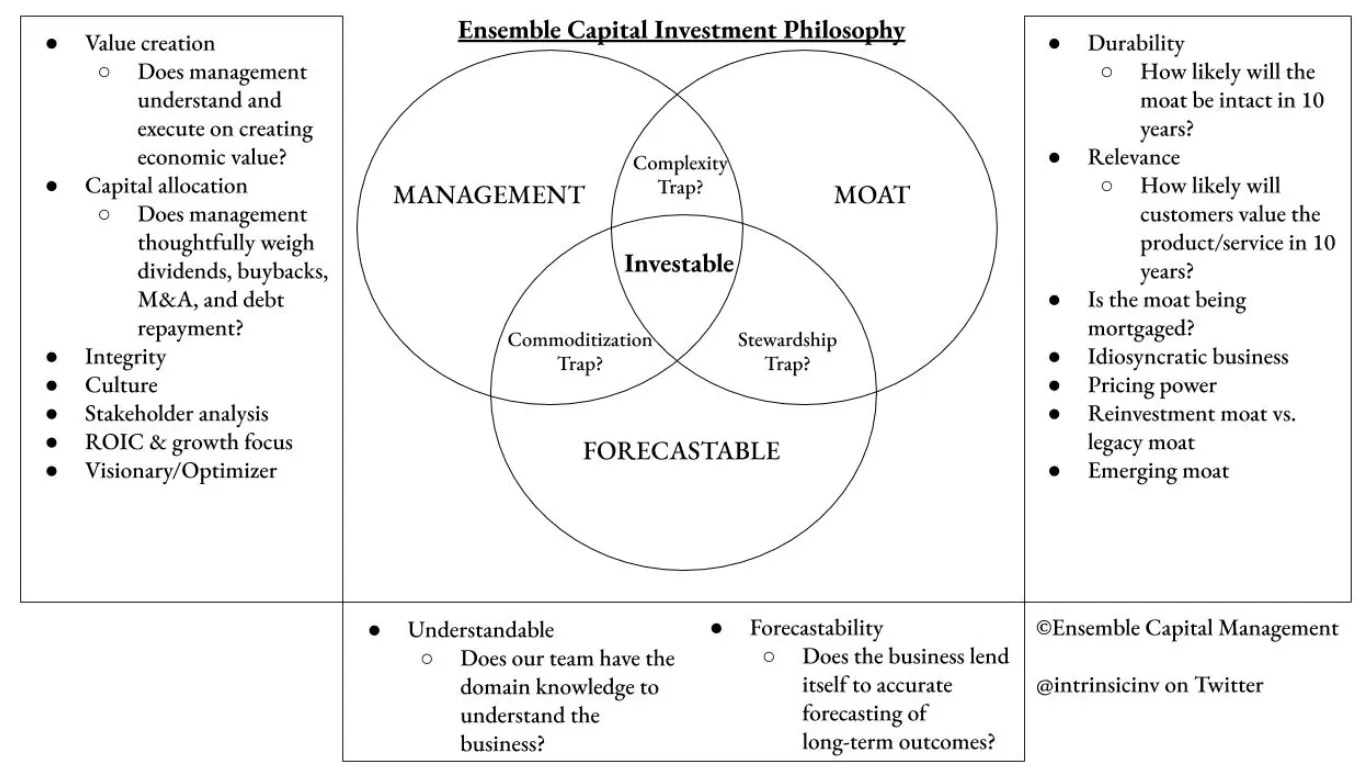

[00:02:33] Mokaya: Thanks Sean for that. It was not paid, I can confirm. Maybe give us perspective on how does Ensemble Capital allocate capital and what's your process? I know you have a Venn diagram where you have three circles and there's one at the center. So maybe you can give that as a way of introduction to listeners who don't know how you invest your money.

[00:02:52] Sean: Yep. So our portfolios are made up of typically between 20 and 25 securities. When we're making an investment in the company, the intended timeframe is effectively perpetual in the sense that when we are investing in a stock, we are assessing the idea that the company is going to produce the cash flow to drive a rate of return that we expect. So rather than thinking about where might this stock trade in three years and whether we can make a profit between now and then, we're thinking more as business owners and saying, based on the current valuation of this business and the cash that it produces, and we believe it will produce in the future, what is the cash rate of return I'm going to earn if I were to go out and buy the whole business? We're buying a pro-rata share of that business, of course. But that's how we think about it. And we've held securities in our portfolio for over a decade. And our average turnover of companies in the portfolio is only 10 to 15%. We do a pretty aggressive position sizing framework that listeners can pull up on our blog and Intrinsic Investing and read about. So we have a higher turnover and trading between our holdings. But I give you that context in the sense that we're really trying to think about the long-term economics of these businesses and the evolution of their competitive environment. And so the Venn diagram you asked about is we're looking for businesses that are very competitively protected, have some sort of moat that protects their business, and that they have a moat that's going to be relevant over the long-term. There are plenty of moats out there that protect a business that is in perpetual decline and maybe they can't be competed with but you have declining cash flows and you got to pay attention to that.

We're looking for management teams that recognize that their role is to generate value for all of their stakeholders, and that includes shareholders, of course, but in order to do that, you have to create value for your employees, your suppliers, and your customers. And so we're thinking about all of that. And then we spend a lot of time just thinking about, is this a business that we can understand? There are a lot of businesses out there and sometimes complex businesses offer great returns, and sometimes simple ones do, but the key thing is that are we positioned to understand it well? And there are times when we've passed on a company just recognizing, you know what, there are other investment teams out there better positioned to understand this business better than we are. And we got to take a pass on that because it's hard enough to understand the businesses that we do understand really well. And so that's the Venn diagram approach. And then as it relates to earning season, as much as we're long-term focused you got to be paying attention to what's going on in your companies all the time. And quarterly updates are one snapshot into their business. But even on an inter-quarter basis, things are changing all the time. And I think the goal is not so much to try and call the quarter, we don't trade in and out of stocks around quarterly earnings, but to understand how is this business evolving and which of our expectations are proving to be correct, where is the business operating differently than we expect and what that means for our longer-term thesis.

Focusing on the Long Term While Engaging with Earnings

[00:05:37] Mokaya: In terms of quarterly earnings, there is a lot of noise usually around the time. The analysts consider estimates versus what the management is saying and all, so you see a lot of trading in and out of stocks around this period of time. And sometimes stocks sink by a lot like one of the stocks you own Netflix, sunk by around 20% two or three quarters ago when they showed a decline in terms of transcribers. So you have to insulate yourself a bit from that so you can think about, okay, this stock has a moat, has a good management team, it's forecastable for us. How do you then insulate yourself so that you can keep that patience to help you hold the stock long-term and not just trade in and out of the stock during the period? How would you advise maybe investors to go about that and how do you go about that yourself?

[00:06:23] Sean: The first half of this year was particularly challenging in that respect, in the sense that there were times and, as from January through June, I guess really, where there were businesses that we believed may well miss earnings estimates, and yet we felt the stock was deeply undervalued relative to the longer-term trajectory of earnings and cash flow and all of that. And, when the market is trading down, you can think to yourself, God, I just got to get out of the way. But of course, what you have to be able to recognize is that they're going to miss. Other people don't know that because a lot of sell-side estimates can get stale, especially in a market environment like this, which is why you see companies miss and the stock goes up because everyone knew they were going to miss, and it's really a struggle.

We just honestly just don't try and trade around other investors' expectations. And I think this is a key area to think about where your competitive advantages as an investor are. For us, we believe that we are competitively advantaged in understanding the competitive advantages of the businesses that we own and that therefore we are competitively advantaged in understanding their long-term cash flow production and evaluating what is that worth to us as investors. We don't think we're competitively advantaged in guessing what other investors' opinions will be to news flow that comes out in the short term, and that's what trading requires. You have to be able to predict future information better than your competitors and then also better predict how other investors will react to that information. And to us, that's really about crowd psychology. So if you are somebody or a team that says our expertise is doing crowd psychology analysis of other investors, by all means, trade the quarter. It's just not what we do.

Macro Perspectives

[00:08:03] Mokaya: And in terms of macro then maybe let's start from a higher level view. I know you don't trade in and out of macro because you want to hold long-term, but then you are also in an economic environment that is slightly changing from a period where there is a lot of capital available and nowadays capital available but at a higher cost of capital, how do you think about the current economic environment in terms of what relates to cycles and your long term investing view? Is it time to go into the market and pick a few stocks that you may have been on your watch list for so long?

[00:08:33] Sean: I think a lot of long-term oriented investors have often taken the view that they're macro agnostic, that we don't really know what the economy's going to do, and we just focus on companies. But I think that's actually a disingenuous point of view because all companies are operating within a macro environment, and I think the only real choice for investors is either to make explicit what their longer-term macro assumptions are or hide it from themselves and implicitly embed it into some assumed PE ratio or something like that, or some sort of growth rate. So when you say that a company is going to grow 5% a year for the next five to 10 years, or 8% a year, or whatever the forecast is, whether you like it or not, you are assuming something about the macroeconomic conditions in which that company's going to be operating. And so for us, I think that we probably pay a fair bit more attention to macro and are more aggressive in making explicit our macro assumptions. It's not something that we do publicly very much, but in terms of driving our own longer-term expectations but what we don't do is try and call the short-term path of the economy, right? What is GDP growth going to be next quarter? What's inflation going to be next quarter? I don't know.

And you don't know, and nobody on this call knows. The feds are reserved, for all of the criticism they get, they are some of the most talented economists in the country who are resourced with literally unlimited spending power and literal access to private streams of information that nobody else has, and they don't know what's going to happen. And so because of that, I think that most investors, unless you decide that you can trade the macro and guess macro yourself most fundamental equity investors are best served by thinking about what are the long-term behaviors of economics and investing. Will real GDP average 2% as it did in the decade between the financial crisis and covid? Or will it average more like 3% as it did for the 50 years prior to the financial crisis? Will inflation average 2%, which is the fed's target? Will it average 3%? This is actually what was the average in the 1990s, which was a great year for the great decade for the economy and stock market and all of that. And yet you had inflation levels, which today we would say that's too high. And then interest rates, right? There's a lot of research that has shown over the last 40 years that low beta stocks, bond proxy type stocks, consumer type staples, and sorts of boring stocks outperform high beta stocks. But you have to recognize that occurred during a period of declining interest rates, perpetually declining interest rates, and during the period interest rates rose, those stocks mostly did poorly. So if you believe that interest rates may stay at current levels or trend higher over time, you need to recognize that behaviors of equities that occurred during perpetually falling interest rates may not replicate themselves going forward. So I think you really do have to have an explicit view of the longer-term macro and also not fool yourself into thinking you can guess, what is the CPI print going to be next month.

[00:11:37] Mokaya: I agree with you. One of the pickings we had from the earning calls was Apollo CEO saying that a lot of the investors that have come into the market in the last 10 years will maybe learn the very harsh lessons that sometimes a rising tide picks everyone going up, but then when the tide goes down, then you realize you're swimming naked and all. So I think as you say, market beta is something that we should really pay attention to if I get that right. Correct?

[00:12:00] Sean: I think that's right. I think a lot of accolades of Warren Buffet and I would echo that as well, we've looked at a lot of his comments in which if you spend 15 minutes a year thinking about the economy, it's 14 wasted minutes or something like that. And yet if you look at his investments, they are all very much driven by economic growth. And then he makes investments like recently in Taiwan Semiconductor in Taiwan. And whether he says it or not, he has a view on the geopolitical implications of what's going on with China and the US right now. And so for all of the talk he might give to focus on individual stocks, you can't predict macro, you can't predict geopolitics and all this sort of stuff, he's right in a philosophical sense, but in a very real sense, he makes very specific investments that are underpinned by an economic outlook, whether he shares it or not. But what he doesn't do is he doesn't say, I think there's going to be a recession this year or next quarter, or, that sort of thing. I think that's the right approach.

The Ensemble Approach to Investing

[00:12:58] Mokaya: I may have forgotten maybe to start with this what got you interested in investing and what’s your journey to being part of Ensemble Capital, and Intrinsic investing blog?

[00:13:07] Sean: I was just one of those young teenage kids that found a book about stock picking and fell in love. The first book I read was a terrible book. I won't even mention it because the author who was also a teenager turned out to be a fraud. It was like in the ‘90s when lots of people were speculating and I read this book was just amazing. And then luckily very quickly found other books like Peter Lynch's One Up on Wall Street and some of Warren Buffet's writings and so by the time I was doing anything professionally, I'd learned what were the good ways to learn about investing. But for me, it was always just a fascination with business and how business works. My father was a sociologist, and my mother was a psychologist, and initially, when I was young, they both were like, you want to go into finance like that, where'd that come from? But today I recognize that companies are just collections of people. The legal entity of a company is just a fiction that we create to organize the activities of people and groups of people are best understood through a psychological and sociological lens. And so I think about the work that I do as very much a humanist kind of social sciences work, a liberal arts approach. There's one of my favorite books I'm investing is by Robert Hagstrom, called Investing: The Last Liberal Art. And I think that I was raised with a certain lens on the world, and then I reoriented those lenses towards money and finance. By the end of the day, it's about how people operate. How do they create value in the world? How do they achieve their goals?

Ferrari and Luxury

[00:14:32] Mokaya: At this point, I want to now dive deep into a few of the stocks that you own, which also happen to interest us a lot. I'll maybe pick your brains on Ferrari, Netflix, Home Depot, and MasterCard. Ferrari as relating to luxury, Netflix as relating to streaming, Home Depot, which reported earnings I think yesterday, as relates to retail and consumer, and MasterCard and payments. I think those four. And then if you have any other thoughts outside those, I will also ask questions. And at this point also I want to ask the audience if you have any questions, you can check our pinned tweet. You can write your questions below. You can DM us. You could also just ask to speak at some point, we are only here for the next 45 minutes. I want to start with Ferrari. It's a luxury brand. It's a tough time for most consumers, especially low-income consumers but then you have Ferrari reporting, which is one of the companies that you consider to have a very strong moat and I want to read a quote from the earning call of Ferrari the latest one. The CEO says, "We offer the possibilities to some customers that were selected through a lottery to drive the cars for around 40 kilometers. And I cannot share with you, but they are videos of people that are really crying for the emotions that they experience in terms of just being or driving those cars." Speak to me about maybe all your pickings from Ferrari, the earning calls, and how they're doing in terms of the long-term perspective that you own them for.

[00:15:51] Sean: I think that one of the key things to recognize about Ferrari is that despite the fact they sell cars, they're really not a car maker. And if you look at their financials and compared to other car makers, you'll recognize that they're doing something very different. It's not just that they're like a better, more profitable car maker, it's that at the end of the day, they are not selling transportation. And that's what car makers sell. They sell a form of transportation. Ferrari is selling quite literally hopes and dreams and self-images and all of these elements that are critically important. One of the things I think that many people don't always appreciate is they also offer membership in a global club of ultra-high net worth individuals, and that has real value and benefits to those members. Now, I'm not a car buff myself. Honestly, if you gave me a Ferrari, I'd be like, that's cool, but I really don't want to drive this thing around. And so I think our job as investors though, is not to say what do we like in the world or what's best for us, but are these companies meeting the needs and desires of their customers, right? And so with Ferrari, given all of the concerns about a recession, you could think to yourself, oh my gosh, how could you own a car company going into a recession?

But in 2008, and 2009, Ferrari saw only a single-digit decline in unit sales. And there are two pieces to this. One, their client base, by and large, even in a recession, even after a big decline in equity values, still has enough money to buy a Ferrari. And you have to get on this wait list. You have to be given permission to buy one, right? And so when you get to the front of that wait list, if it's a recession or you're worried there might be a recession, you as a buyer also recognize that if I don't buy it, I can't get back on the list. And if I'm going to do it, I should do it now. And so what Ferrari was talking about on their most recent call was that their order books are stronger than they have ever seen them before. And you think, how could that be, given all these worries about a recession, and yet at the end of the day they have these products that their customers love and their customers still have a whole lot of wealth. They also talked about supply chains starting to improve. And I think that when we think about inflation, it's easy to abstract it away from the actual impact on individual companies. But things like auto parts in the auto industry was one of the most heavily impacted. Now, Ferrari makes relatively few cars. They sell, 10,000, 11,000, and 12,000 cars a year. And so there's a lot more ability for them to control their supply chain. They're just operating at a smaller scale than most of their other competitors. But I think that the key message from the earnings call for them was that ultra-high net worth people are still spending on the things that they need and desire.

[00:18:39] Mokaya: That's amazing. I think there's a statistic you shared in a recent write-up that you wrote that they shift around 10,100 cars is it in 2019, and that's against the number of visitors to their museum around 600,000. So it shows you there's a huge difference in terms of interest and actually how much they deliver. Of course, the order book is really high. A quick question I wanted to ask. A couple of months ago, the Ferrari CEO was heard saying that they will never be a self-driving Ferrari and I think the quote was, “No customer is going to spend money for the computer in the car to enjoy the drive. The value of the human as the center is fundamental.” Any thoughts on that, does it fit into the moat in terms of what Ferrari has in the mindset of the consumer?

[00:19:25] Sean: Yeah. I think the biggest risk to Ferrari longer term is changes in how we interact with automobiles. So the shift to EVs is a big deal and the shift to self-driving is a big deal, and Ferrari needs to navigate both of those things. Now because a Ferrari is not primarily a form of transportation, you're not going to say I'm going to take a self-driving car to commute back and forth to work rather than drive my Ferrari. It's just they're not substitutes. It's a totally different sort of thing. It used to be that Ferrari years ago was a lot more skeptical of EVs. That they were, “We'll do it when we need to.” Now they, like every automaker in the world is going all in on EVs over time. And I think that it's going to be an important challenge that they need to maintain their brand value even as the concept of automobiles change. So if you think about the sound, like the roar of a Ferrari, EVs don't naturally make sounds. Most EVs makers are making them make sound, but will that be experienced as artificial in some way? That being said I recently was walking with my son, a teenager, and an electric vehicle, kind of a sports car pulled away from a car right next to us, and it made this sound that was a little bit more like one of the speeders from the Star Wars movies is like Zoom, spaceship futuristic noise. And my son a teenager was like, oh, doesn't that sound awesome? It's so silent. That's cool. And I'm thinking to myself as an older person I expect a roar of an engine is what's cool, but once upon a time, a century ago, the chew of a chain of a train whistle sounded like futuristic stuff. This was modern, today it sounds old-fashioned, right? So I think how all these changes will be a challenge. It's the primary challenge for Ferrari. And when it comes to self-driving, I don't know. The CEO might change his tune in the years ahead. People care a lot about image and even if you have a self-driving vehicle, you might care a lot about the brand of that self-driving vehicle. But I do agree with them fundamentally that Ferrari a lot of it is about the experience of driving. And you have to believe that humans are going to continue to care about that long into the future.

[00:21:31] Mokaya: I think the beauty of listening to earning calls often is also you see these changes in trends in terms of management. I've been following Ferrari for a while, as you said, the CEO some quarter ago said we are not interested in EVs but then again like they're full-on EVs this year. It seems like they're very nimble in terms of how they're able to listen to the consumer, to the tastes and preferences that are out there, and perhaps change also how they do some things here and there to keep tabs with the consumer, but still retain that brand value if I get it right.

[00:22:01] Sean: I think that's right.

Mastercard and Payments

[00:22:02] Mokaya: The next company I wanted to have a look at is MasterCard. And one thing about some of these companies, you've owned them for long. MasterCard, I think you've owned 10 plus years, what’s the moat there, and what is your takeaway from the Q3 earnings for MasterCard?

[00:22:17] Sean: So MasterCard, much like Visa, the competitive moat is a classic network effect. So the reason that you carry a MasterCard or a Visa is because you know that quite literally everywhere you go will accept it as a form of payment. And the reason it's accepted everywhere is the merchants know that quite literally everybody, every one of their customers is carrying one of those cards in their pocket and can pay with it there. And so it's this minor miracle if you think about it, you can jump on a plane and fly to Peru and get off the plane, walk out of the airport and walk 10 minutes and walk into a store, pull this piece of plastic, swipe it, they don't even know you and they give you stuff.

It's a miracle to actually be able to have these abilities to transact around the world with people we don't actually know. And everyone just trusts the money is going to be there. I don't know this person, but they swiped that piece of plastic, so we're good. And we saw last year this whole assault on their network with the buy now pay later providers looking to use a different approach to payments. And of course, that has basically crashed and burned. To us, we think about a moat attack. So when a company that has a moat has well-funded competitors attack that moat and fail, it tells you something about the strength of that moat. Some moats are untested, they're thought to exist and then somebody runs them over one day and breaks them down.

Moats are not invincibility cloaks. So that's the core moat for MasterCard. And what they said in their earnings call is the same thing that Visa said and the same thing both companies have been saying all year long, which flies in the face of so many of the macro worries that we all have. Despite those worries being very reasonable, Mastercard, and Visa have been saying, every quarter, including their inter-quarter updates, like spending, just continues. Consumers all around the globe appear to be quite healthy. They're still spending, and still growing. And we all read the macro headlines and we're worried about next year and maybe it slows down and we probably have a recession, but it's not here yet. And in the US with 70% of GDP coming from consumer spending, it really tells you something powerful, that here we are in November with a whole year of recession worries and real slowdowns in the economy. And yet consumers are spending at the same sort of run rate that they have all year long.

[00:24:38] Mokaya: A quick quote from MasterCard is, “What we had shared at our Q3 earning call is that we expect a resilient consumer through the end of the year.” And through the first week of November to date, they're still seeing the same. It's consistent. And I think the same thing that you say that the consumer is still strong and still resilient despite the fact that most people are expecting them to be shaken. But then something interesting is that MasterCard gets a piece of the transaction every time the consumer spends. So it doesn't matter where the consumer is spending as long as they're spending. In the pandemic, they were spending on the kind of discretionary items and now they are on travel experiences and MasterCard is in all those places. So anywhere you go, everywhere you go, it seems like these two, MasterCard and Visa are very strong. And perhaps I could share my experience from being in the BNPL area. I worked on that for a year or so with Klarna and I realized at the end of the day that the core people in this segment, the core and key players who may not be challenged have to be MasterCard and Visa. It doesn't matter who the new player is, they still take their cut of whatever spending that is going through the system. You may label it BNPL, or you may label it anything else, they still get their cut. Do you get that same sense when you study these companies? And by the way, why did you choose MasterCard over Visa?

[00:25:56] Sean: On the first question, we first invested in MasterCard I believe in 2009, and we also owned Apple from 2009 through 2018. So most of that time period that we were owning both stocks, and ahead of Apple launching Apple Pay there were a lot of discussions around how cell phones could disintermediate the credit card companies because we would all just pay on our phones, right? And we as Apple shareholders recognized wow, Apple has all of these connections at the time through iTunes and the ability to set up debit cards, which still is Visa, MasterCard but maybe it's a lower profit than on credit card transactions. And maybe Apple could go so far as they've been making efforts to now to establish more or less their own bank and things like that. And yet each innovation along the way consistently with innovations in the user experience, but still running on top of the MasterCard and Visa rails. So even if you get an Apple credit card and use Apple Pay, that's a MasterCard. It's a Goldman Sachs credit card co-branded with Apple, with MasterCard processing the transactions. And so I think we've seen even the most well-resourced, and one of the most ambitious companies in the world say, let's just build on top of MasterCard, and Visa rails. And for all of the things you see about 2% fees on credit cards, MasterCard and Visa get like 10 to 20 basis points, the rest of it is going to the banks. And that's a whole different set of questions, but in my view, the fees that MasterCard and Visa charge for actually facilitating this whole network is a total bargain. And you hear merchants complain all of the time about how high fees are, and yet those same merchants are more and more telling their customers, you can't use cash here, you have to use a card. Because they know that using cash doesn't have an explicit cost, but it has a whole bunch of implicit costs, your employees steal from you, there's miscounting, you got to handle all that money, you got to have it moved around, and shipped places. Get Brinks to come in and move your cash out of your store and bring it to a bank.

And so they're a real cost to accepting cash. And in our view, the cost associated with the processing cost that MasterCard and Visa are charging is really a bargain in a lot of ways. And then you asked why we own MasterCard. Some of it is just history. When we first invested in it, MasterCard was cheaper and had less exposure to debit. And the view was that was bad. The fees could grow faster because debit was a faster-growing category. It turned out that debit value was going to decline because the Fed was going to come in and reduce how much you could charge for debit.But we just saw MasterCard also as being much more truly international in emerging areas where there's more long-term growth. Their management team is a collection of people from all around the world with diverse backgrounds and experiences. Visa's much more of a US-centric company that's now also European-centric. And so it was just a different sort of investment, but within our entire portfolio, MasterCard is probably one company that we could swap it out with Visa because this is truly a duopoly. So most everything that I say positively about MasterCard would also be true of Visa. But now having owned it for a decade, we have real institutional knowledge about MasterCard's business that is superior to how well we could ever know Visa. And so to switch we would really need to have a significantly improved forward return outlook for Visa, not just a margin one, but one that was significant.

[00:29:17] Mokaya: There's a brilliant quote I wanted to read which I got from the earning calls, a while back. I think it was Visa but it equally applies to MasterCard and they say, “We've always thought of ourselves as the enablers of disruptors. We are the ones who are probably able to allow disruptors of scale.” And at the end of the day, once these disruptors especially in the payment system scale, MasterCard and Visa, once again take their cut, you think of them mostly as toll road operators. So at the end of the day, whatever road you build, they're still right there to pick up a piece from both sides of the divide. Any final thoughts on MasterCard before maybe we switch over to the other two companies I wanted to look at before we finish?

[00:29:57] Sean: Just briefly, I think most people have this incorrect view that when a recession comes, the consumer gets decimated because you see certain consumer discretionary stocks decline a whole lot or their sales fall and things like that. But at the aggregate level, in a recession consumer spending only falls a couple of percentage points. And so that certainly would be a slowdown versus what's happening now. But when thinking about recessions, I think it's important to recognize that consumer spending is far more stable than most people appreciate. Because any decline in GDP of any kind of single-digit magnitude is a recession if it persists for a little while. And yet consumer spending is most of the US economy and most of the economies were MasterCard’s playing. And so I think that you need to recognize that there would be a slowdown in growth that would then reaccelerate on the other side of the recession. But this is not like a consumer discretionary time where consumers spend on all different sorts of things. And this is one of the quotes that MasterCard has been talking about, a company like Target might be seeing these huge rotations in spending between less spending on grills and flat-screen televisions, and more on luggage, kids' toys, and stuff like that. MasterCard doesn't care, it's getting a slice of the spending no matter where it goes.

Netflix and Streaming

[00:31:11] Mokaya: At the end of the day, I think that's what matters. I want to switch to streaming a little bit and maybe get to discuss some of the stocks that have been beaten down a bit post-pandemic. What's your take on Netflix now, especially given the fact that there is a solid competitor in Disney? But then at the same time, they're also switching to ads and adding an ad tier to their offering. What's your thought about their moat and maybe how it's been challenged or changed now? They're also one of the companies, maybe I could pick something to compare to, especially Ferrari, the Ferrari CEO, for a couple of quarters was saying we are not interested in EVs but then suddenly they switched to EVs and Netflix has been for a while saying, we're not interested in ads but now this past quarter we heard that they're actually introducing an ad tier. They have also been saying they're not very interested in sports but then sports is also one of the things that they're also considering right now. What do you make of some of these changes that have happened and especially the last two or three quarters for Netflix in terms of transforming the way especially investors view them versus how you view them yourself?

[00:32:14] Sean: So Netflix has been a very challenging stock to own this year, and we came into this year with it as one of our larger positions. And as everybody knows, it got absolutely annihilated in the first half of the year. And while it's come back dramatically it is still down significantly for the year. And I think that the way we think about Netflix over the long term is we believe that the shift to streaming is absolutely inevitable. And even today, for the first time in the United States, you've had streaming minutes viewed exceed linear minutes viewed for the first time, and that is only going to continue. So there is an enormous ongoing push toward streaming. And then the question becomes, does Netflix maintain or increase their position within that bundle? And one thing that we can see again on minutes viewed is that since the end of last year when the stock was a whole heck of a lot higher Netflix's share of streaming minutes versus their main competitors has remained relatively stable and even increased to some extent depending on the exact timeframe that you use. So they're not losing share of attention, but what they did lose in the first half of the year was their churn increased and their gross new signups decreased. And so you had in the fourth quarter of 2021, they added 8 million new subscribers, which puts them at a run rate of say, 13 to 14% annual increase in subscribers, which is what their multi-year run rate had been running at for some time.

And then all of a sudden they print, I believe one and a half million in Q1. And then they went negative in Q2 and the stock fell to 170 and the narrative suddenly became growth is done for good, that this is a business that's going to go into secular decline. And that's what we think is just fundamentally wrong. If you look at the data, all stream providers have seen a slowdown. It's clear that inflation is pressuring the very consumers that are most likely to churn. For somebody like my household, we just watch Netflix regularly. I wouldn't think about getting out of my budget to save money. It's just a very small thing but for a significant number of people and a $15 a month subscription, and then the gasoline fill of your car doubles or something, you're just like, I got to cut back somehow. And that was clearly one of the ways that people chose to do that in the second half. So in Q3, they announced a return to growth and then provide guidance for Q4 of accelerated growth. And if you put those two together, you can see that it implies a run rate of six to 7% annualized user growth. So no doubt subscriber growth slowed, the question is, what is the longer-term trajectory?

We still are operating in a global world of recession fears, economic pressures and inflation, and yet the company has already re-accelerated, assuming they hit their guidance in Q4. Already, re-accelerated to a six to 7% annualized growth rate. And that's just the user growth and the pricing growth on top of that. We do think that over the next say five plus years, we're going to all look back and say streaming kept going, and Netflix maintained their central position. Yes, there are other streaming services, the thesis was never that Netflix is going to be the one streamer to rule them all, but they are the core of the streaming bundle. And that most all households will stream and most all of those households will have Netflix as part of the streaming bundle.

[00:35:38] Mokaya: And what role would the ad tier play in this new outlook for Netflix?

[00:35:44] Sean: So when the business first slowed down and they started talking about an ad tier and started talking about other sorts of things like cracking down password sharing, where in the past they had even joked about people sharing their passwords, tweeting things like sharing your Netflix password is true love and things like that, and then suddenly they seemed to have reversed on those. And I think that the bearish take on that was that, oh my gosh, they're panicking. Things have slowed down. They're going to try things they said they've never done. But if you have a sense of history, you know that Netflix has done this exact same thing in the past. So when they tried to split off their DVD business from the streaming business, the initial way that they did that was received with a thud. Consumers were livid about it, and they ended up turning the whole thing around in just a couple of months. And when that happened, this was before we owned the stock, we first invested in Netflix in 2016. I naively wrote them off this is a bad management team. They made this big decision, it blew up in their face and they’re changing everything, which they clearly are in disarray. But as we followed the company longer, it came to appreciate, wait for a second, every management team we invest with is going to make mistakes that are inevitable. The question is, which ones react quickly to correct those mistakes and which ones double down on their mistakes? And so with Netflix, I think we have a management team that has a history of reacting incredibly quickly to changes in the market environment, and changes in their understanding of the business. And the fact that they rolled out this ad service in about six months is mind-boggling, as the speed with which they are able to operate. So they announced that they were going to do it after Disney and they rolled it out sooner than Disney did. It's an incredible shift.

And so is it the right move or is it desperation? And I think as a consumer that I haven't watched advertisements in videos for so long in streaming that I find them unbelievably disruptive, and I would never think I want to save three bucks a month or five bucks a month to avoid watching ads. even with Netflix only having three to four minutes of ad load per hour, which what they said they were going to hit, or it was four to five minutes, I think you're still talking about getting paid about 25 cents an hour to watch ads versus paying up for the ad for each tier. And yet we can look at Hulu and see that some people make that trade-off. And I think that if you understand that Netflix is reacting to consumer demand and consumer interest and giving people what they're asking for, you say why wouldn't they do that? And so the one worry that we have at the ad tier is that today you and I are the customers of Netflix, and they're making content for us, but in an ad-based business, the advertiser is the customer, you're making content for them. If Netflix were to shift its business model so dramatically that the advertising tier subscribers were like a majority or some big percentage, it would start to bring into question, can Netflix keep making top-tier content or are they going to dumb it all down into a pre-streaming era, mainstream television thing where all the shows were made to be not offensive and just make sure that the advertisers didn't get pissed off in some way. That would be terrible for Netflix. We do not believe that they will do that, but there is a risk of going into the ad business that your customer is changing in that way. But assuming it remains a relatively small portion, it does increase the range of people who have access to it. And why not? I mean that if that's what people want, why not give it to them?

[00:39:09] Mokaya: One of my pickings from the earning calls of Netflix is that they have great admiration for Disney especially. What do you make of the challenge from Disney? I know Disney is more family focussed but what do you make of the challenge that Disney provides to Netflix? Is it the one that would make Netflix have a sharper edge or one that maybe dominates Netflix at some point?

[00:39:33] Sean: So it's not like competition from Disney's new. You can go back and look at what happened when Disney Plus was first launched, and we wrote about it in real-time as that was playing out and it was clear that Disney Plus had enormous success in signing people up, but it appeared that only approximately 5% or less of new Disney plus subscribers, this is like in the first year or two of launch, canceled a Netflix subscription when they signed up for Disney Plus. For the most part, it's a compliment. For the most part, these other streamers just bring more content into the field to the extent that a customer says, why do I need linear television anymore? If I had Netflix, and maybe there's only Netflix, but there's stuff I want to see on linear television. But now with these other services, including Disney's package, you can start getting more and more content very quickly, you are like, why would I have linear television And yet there's still an enormous number of people paying $100 a month for cable television when they can basically see almost all the same stuff in a cheaper, better format with streaming unless you care about live sports or live news. Live news is something that older Americans watch and every year fewer and fewer people care about that. And then live sport is an important category. And Netflix had recently changed how they've talked about it to some extent, but there's no doubt that's an important long-term category and how that gets met and served may be different. And we think Netflix may play a role in that, they've said it and we think it's true. They're not going to be where you go watch the Super Bowl even far into the future.

[00:41:00] Mokaya: So my takeaway from that is, of course, Netflix they're pretty adaptable to what they do, and that comes a lot from reading all the transcripts that I've read since I think 2016/ 2017 thereabout. So following them I learned they listen very well. They don't say they would never do something, but they also are very adaptable in the sense like, if they see a consumer who wants an ad tier, they'll add it. If they see someone who wants to say sport they'll get the sport and put it on their platform. They're not afraid to try out new stuff and that's what you want to do. And another takeaway, of course, is what you said about them, they will make mistakes. Most companies will, and you just have to be swift in terms of, okay, there's a mistake, let's change, let's try and do something different.

Home Deport and The State of Retailers

Maybe in the next few minutes, the question I wanted to ask more was to do with Home Depot they reported yesterday. What were your key takeaways from earnings? I know one of the things I picked was that inventory grew quite fast, around 24% year-over-year, but then sales were up around three or 4% there. So in terms of the inventory when you look at, let’s say Walmart, they have slow growth. They've dealt with a lot of the inventory that they had. Does that worry you about home Depot in terms of your long-term thesis around the company and how they operate? Maybe you can speak a bit about what they do for someone also who does not know what they do.

[00:42:13] Sean: Home Depot provides products and services related to home maintenance and remodeling home improvement. And about half of their revenue comes from do-it-yourself, homeowners, who say, I got to fix the light on the back deck and they run out to Home Depot to pick something up. And the other half comes from pro-contractors. The pro-contractors historically are not going to Home Depot to buy all of the building material for a big project, but when the project's ongoing they're sending runners out all day because you could be working on some big project and you realize, oh, we don't have this particular bolt that costs $1.50, but we can't keep moving on this job until we have that particular bolt, and so you have to go out to Home Depot and get it. 90% of Americans live within 10 miles of a Home Depot, which means contractors are always within five, 10 minutes drive of a place to go replenish whatever parts and supplies they need. And given the wreckage that has occurred in home transactions, and home sales this year, as interest rates have skyrocketed, I can imagine some investors might believe, oh my gosh, sales have to go down a whole lot at Home Depot. But the company, this is years ago when there weren't so many worries about higher interest rates, they would still get questions about the rise and fall of interest rates. And at one point, on one of their calls, they said something to the effect of we have tried every way to find a correlation between interest rates and our business, and we just can't find one. And I think at the end of the day, you have to recognize that maintaining a home is like a staple sort of behavior. Oh, I got a leak in the roof, oh, I've got this deterioration going on in my house and need to fix this stuff and maintain it.

Of course, it ebbs and flows with the economy. But if you just look over the last decade between the financial crisis and Covid, you can see that Home Depot's revenue grew at a 5-7% rate every year with very minor variability, despite the fact that the economy did ebb and flow, and interest rates did rise at different time periods. And so I think that today what you have is you have an American homeowner base, two-thirds of all Americans own their home. 40% of them own their home outright without a mortgage, and the other 60% have a mortgage, of which 95% of them, it's a 30-year fixed rate mortgage with a 3.3% average interest rate. So those homeowners, they're not experiencing inflation within their cost of shelter, which is one of the big drivers of inflation for renters right now. And they generally all have jobs. They've been getting raises, they've saved a lot of money during COVID, and so you have an incredibly healthy segment of consumers. And suddenly some of them are saying, oh, we wanted to move to get an extra bedroom because we've got a new baby on the way or something. Or, oh, I got to work from home and my spouse does as well, so we need to move into a bigger house. And suddenly they can't because they own their house with a 3.3% mortgage rate. If they go buy a house with a 7% mortgage rate, they have to buy a smaller house unless they've just got tons of money on the sidelines. And so that money needs to be re-channelled into home improvement in some ways for times that can work. Let's add a bedroom to the house. Let's go up a level, let's make some sort of shift in the way we have the house set up.

So we do think that the longer term is very well positioned for Home depot and home improvement. What we're seeing in the very near term, which has just been reported is continued sales growth. The pro-contractor has been the major contributor to growth for a number of years now because the do-yourself homeowners we all splurged on a grill and, something for our back deck in 2020 when the only thing you could do to socialize with your friends and family was do something outside. But that has been mostly coming back. They don't report do-it-yourself versus pro-sales, but our analysis suggests that do-it-yourself homeowner spending has declined on a year-over-year basis every quarter since the second quarter of 2021. All of their growth is empowered on the pro side of the business. But what's interesting is right now is that pro is slowing down as everybody paying attention should expect that it would be, and yet do-it-yourself spending appears to be picking back up. And Lowe's which has more exposure to do-it-yourself just reported this morning. They actually raised Lowe's guidance. And so the do-yourself homeowners, we think their spending surged in 2020, but it's fully reverted to the trend. There's no elevated spending that's been going on. And now consumers are continuing to pick back up their spending on home improvement. The big debate on the stock really is what pro-spending is going to be like over the next year or two, especially in a recessionary environment. And as of right now, pro-contractors, and this is what Home Depot and Lowes say, and you can talk to them yourself, they say the same things, we still have long backlogs of projects to do. So we will see, it would not surprise us if you see a decline in revenue earnings for Home Depot next year if you assume that you have an increase in unemployment of some magnitude. But when you think on a longer-term timeframe, you know there's going to be a lot of money spent maintaining the US housing stock. And Home Depot is incredibly well-positioned to capitalize on that.

Concluding Thoughts

[00:46:54] Mokaya: Perhaps a final question as it relates to the stocks, you have a really interesting portfolio, so two questions. One is about Google and ad spending. Ad spending is a bit challenging as you go. It's a bit cyclical. Companies are cutting ad spending as you going to Q4 this year. Any takeaways in terms of Google and ad spending? One other area that at least the consumer is doing quite well is travel and one of the beneficiaries in your portfolio is booking. Any takeaways from those two? And perhaps three questions. So one is about, as I said, ad spending and Google. The second is about travel and the consumer in terms of booking.com. And finally, also your portfolio looks like holdings of companies almost everyone thinks about, everyone knows, but they don't invest in like MasterCard, Netflix, Google, booking.com, and Home Depot. These are companies that most people talk about. So if you're talking about a moat everyone knows Google has a moat or something like that. But then how come most people don't invest in some of these companies? And why do you think that you have an edge in that regard? Those are the three closing questions.

[00:47:58] Sean: So on the last question around the edge, small undercovered companies should be easier to get an edge in than a big company. And if you're trying to obtain an informational edge somehow, that may well be true. The fact is it's not if you look at the great stock pickers over time that they all made their money in small caps or something like that. Very large business stocks can be very influenced by the sentiment that is way outsized compared to their fundamentals, simply because everybody knows about them already. And in addition well-known companies, people will often say, I don't need to look into it because I already know it. So with Home Depot, a lot of people might say, oh yeah, that's like a home improvement place where homeowners go but half their business is a B2B platform business enabling small contractors. It is a mission-critical input and a small cost base that enables contractors to get jobs done. That is very different than doing head-to-head competition with Lowe's on do-it-yourself homeowners, right? So even these big well-known companies may not be well understood by investors who have not yet dug into all of that. So I just have not experienced in my investing career that it's any easier to outperform the market in smaller, less well-known companies than big companies, but we own both in our portfolio. On travel, it's just clear the travel boom is still continuing. So at Booking, the room nights booked were up 31% on a year-over-year basis, growing faster than Airbnb now up 8% verse 2019, telling you that even though it's booming, we're only at this point at a level of hotel room nights booked that is below what you might have expected at this point if Covid had never happened. So the recovery's still ongoing. You still see recovery going on in Asia and this global travel boom is all happening without the participation of Chinese tourists which is an important part of global tourism. It's very clear that travel is something that humans love and value very highly. They were deprived of it and now they're getting back to what they like to do. Will it fade if we have a big recession? Yeah, sure. When people have less disposable spending, they do less travel, but I think that one that's very clear is that overall global travel trends are not elevated. In fact, they're just barely back up to what you might have expected if Covid had never happened.

[00:49:49] Mokaya: That was very insightful, sean, thank you for joining us today. We hope to have you again another time.

Q3 Earnings Review with Ensemble Capital