In this episode, we discuss the key takeaways from US bank's Q1 2023 earnings and more.

The episode is based on yesterday's newsletter which is available on Substack.

A transcript of this podcast, with relevant images and quotes, is available for all subscribers after the show notes below. Our podcast is available on Apple Podcasts, Spotify, Google Podcasts, YouTube, and Amazon Music.

Show Notes

00:00:00 Introduction

00:00:07 Slowly Declining

00:02:18 What Will the Fed Do?

00:03:18 Banks are Stable For Now

00:04:42 Credit Metrics Look Good

00:06:23 On Semis and Pool Demand

00:08:20 Freight Recession

00:09:10 Tesla Slashing Prices

00:11:06 Big Week Ahead

Transcript

Introduction

[00:00:00] Scott: Welcome everyone to a new episode of The Transcript podcast. You've got me, Scott Krisiloff, I'm editor of The Transcript along with Erick Mokaya who's our lead author.

Slowly Declining

"Specifically on the U.S., we saw a gradual deterioration over the course of the quarter that was building through the end of the quarter, so I’d say if you look at that average rate for the quarter of minus-13, we ended the quarter slightly, slightly higher than that" - ManpowerGroup CFO John McGinnis

We sent out a new issue of the newsletter yesterday and what we saw was that it was the first big week of earnings season for the first quarter, and we saw that the economy seems to be continuing to gradually deteriorate. It's definitely slower than it was even at the beginning of the year. You're seeing banks talk about spending patterns declining, and weakening among the consumer. You're seeing corporate spending patterns decline. And you're also seeing the labor markets start to soften. There were three of the big banks that we've pulled up. So there are weakening trends in the economy that are happening. But compared to a recession, it's actually still a pretty strong economic environment in the absolute, not the relative. And so people are still looking at the fundamentals and thinking it looks like we're going to hit some sort of very mild recession if anything. And the Fed is meanwhile looking at these trends and still feeling like they're not cooled enough in the absolute. And so the Fed seems to still be more hawkish than I think capital markets participants are expecting right now. Erick, any thoughts?

[00:01:12] Mokaya: I think it's a good point to start with the issue of where the Fed is because I think the quote from the Blackstone CEO was very interesting for me. He says that the Fed is likely to pause or maybe go 25 basis points higher, but they're unlikely to pivot as the market is expecting. And for a while, I've also been thinking the same. The market seems to expect a point where the Fed is going to turn, but it seems like from what you're reading in corporate earnings calls so far is that the Fed is not turning. It's not going to turn soon. In fact, if there is anything, they may pause, but not a turn in the sense of the market because market conditions don't seem to allow for it. First of all, inflation is still pretty sticky, very high from what we're reading in earnings calls. And secondly, generally, the bank's issue is still behind us, but still hovering over our heads at the end of the day. So I think because of those two issues, the Fed is kind of, their hands are tied. They will not pivot anytime soon. And that seems to be what the CEOs, at least we are reading from the earning calls are telling us. Is my reading correct there?

What Will the Fed Do?

[00:02:18] Scott: Yeah. That's what I'm thinking as well. It looks like the Fed, even if the Fed is going to stop raising rates or pause on raising rates sometime soon, I think everybody expects that the Fed is still signaling that they expect to keep rates higher for longer and they expect that they're trying to get back to 2% inflation and it doesn't look like 2% inflation is necessarily going to happen this year. And in fact, there are some places where we're even starting to pick up re-bubbling of inflation in a way, like in basic materials where a lot of inflation had been wiped out, there's strong demand for steel for instance, and Steel Dynamics saying that steel pricing has strengthened recently. And so these are the types of things that you could get a little bit of a resurgence or at least not as much of a decline in inflation as people are expecting right now. And then that would keep the Fed, which is already oriented hawkish in a more hawkish stance for longer. And that would be a surprise, a negative surprise for equity markets. So these are things that we're watching pretty closely right now.

Banks are Stable For Now

"Roughly, when you look at the decline in total deposits over the quarter was about 60% happen before March and 40% happened in March." - M&T Bank CFO Darren King

"From March 8 through the end of the quarter, deposit balances were relatively stable, down only 0.6% as inflows from new customers were slightly offset by the impact of clients diversifying their deposits and seeking yield and money market funds consistent with broader industry trends." - U.S. Bancorp CEO Andy Cesari

[00:03:18] Mokaya: Yeah. And maybe we talk a bit about it, because a lot of banks have reported earnings so far. What are your kind of takeaways from the earnings, especially for banks? Because for me, one of the things that has been very clear is that, the bank deposit flows are not as bad as many predicted. It's actually mostly in line with seasonal flows for some of the banks, especially, let's say Bank of America and all. Is that something you also picked up?

[00:03:40] Scott: Yeah. At this point, it looks like the bank earnings that were reported, that the banking stress that happened in early March really was like a very intense storm that passed through very quickly and really only hit the couple of banks that were directly in the center of the storm. And so what we're seeing from banks reporting is that it really isn't touching other even regional banks where people were concerned about contagion. And so basically anybody who wasn't in the eye of the storm did okay. And credit quality still remains relatively strong for banks. Even the deposit outflows for many of the regional banks weren't overly severe although it was accelerated a little bit by SVB, but it was a dynamic that was already in place. MTB talking about, there was a lot of deposit flows throughout the quarter, but 60% of the flows happened in January and February and 40% in March. Just a little bit of an uptick on a relative basis for a bank like MTB relative to the entire atmosphere. But any thoughts from you?

Credit Metrics Look Good

[00:04:42] Mokaya: Just the same, I think it seems as you say, like something happened and then it happened over a period of one or two weeks and then it was done. I think First Republic was reporting yesterday during our recording and one of the things that was noted is that the deposits flow, especially in the months of April, has actually been pretty stable for them. So I think generally it feels like all banks whatever issue there was, it's way behind us. But perhaps one thing that I've noted that strikes me, none of the banks I’ve looked at so far is talking about credit tightening at all in terms of the consumers, like the tightening credit lending standards to consumers. That's been pretty striking. And of course also, if you look at the credit metrics, they're pretty stable. So nothing much is happening, nothing unusual actually. And that's the unusual thing.

[00:05:30] Scott: Yeah, no, it's a good point. I think that people are expecting some tightening conditions, even among the banks, but nobody is directly themselves really saying we're tightening credit. I think the flip side of this though, in terms of banks doing better than expected, is that banks are still gonna be under a lot of headwinds because of this environment and the type of stress that happened over the last month and a half. And it's really all about their cost of funds going up and their profitability is getting hit because of that. And so if you are having to pay more for deposits, it's the net interest margin is stricken for banks. And so banks are not in a strong operating environment, even if they're not succumbing to bank runs. So the financial sector is still one that has got headwinds here as we go into, again, potentially this recession, mild recession, whatever it is in growing headwinds on around that.

On Semis and Pool Demand

[00:06:23] Mokaya: We are slow-walking into a recession, which has been happening for almost a year now. Moving beyond banks, any other things that stood out? I think one thing for me also, TSMC talked about two things. So one is obviously that AI demand is pretty high. The second thing, is they're talking about weaknesses in auto, and that's not something we’ve seen from anywhere else. So they are talking about them seeing a bit of weakness in demand for auto chips. That could be a pointer. We haven't seen anything else. So without supporting evidence, we can actually say maybe not this for next time. Maybe beyond the tech and TSMC area, is there anything else that stood out for you in earnings?

[00:07:03] Scott: Yeah. One thing that struck me was the quote from Pool Corp earnings about swimming pool demand starting to really level out or start to decline because this was something that was so hot during the pandemic. Again, people were spending on homes, people were investing in big-ticket items, improving their homes, and thinking they were gonna spend so much time at home, and now that we're post the pandemic, people aren't thinking that way and quite the same way anymore. And some of the backlogs that were honestly, the swimming pool industry was one place where we saw some of the worst backlogs in any part of the supply chain.

[00:07:40] Mokaya: Yeah, I remember last year it was one of them, because Pool Corp is one of the companies we have followed for the last two or three years, and last year they were telling us how they have up to half a year of orders backlog in terms of pools that need to be constructed. And now things have changed.

[00:07:56] Scott: Yeah, things have changed. So it's really, it's a sign and indicator of just how far supply chains have maybe improved or how much demand has shifted from the pandemic era. And finally, this kind of leading and long-term construction item in swimming pools is seeing its demand curve shift the other way. So that was an interesting one for me there. Anything else for you?

Freight Recession

"As we have discussed shifting dynamics in the market for several quarters now, it should be evident that freight demand is muted, even when taking into account seasonal factors...To start, we're in a challenging freight environment where there is deflationary price pressure for an industry that continues to face inflationary cost pressures. Simply stated, we're in a freight recession." - J B Hunt Transport Services CEO John Roberts

[00:08:20] Mokaya: I don't think I have much, but I think one thing that also I noticed a little bit, I don’t know what to make of it is there's JB Hunt behind talking about this being a freight recession. Do you make anything of it?

[00:08:34] Scott: Yeah, it's interesting. Transports like JB Hunt and FedEx have been really negative for a long time, and it seems like it's something that we should be paying attention to. But again, it may just be the headwinds of the shift from goods demand to services demand, that there were so many goods being shipped around the economy during the pandemic and then as we've shifted more to services demand and then have mild recessionary headwinds going on, the transports are seeing this pretty significantly. They're getting hit pretty significantly by it.

[00:09:04] Mokaya: I think it's something noteworthy because they're pretty negative in their earning score. So I think it could be something to pay attention to.

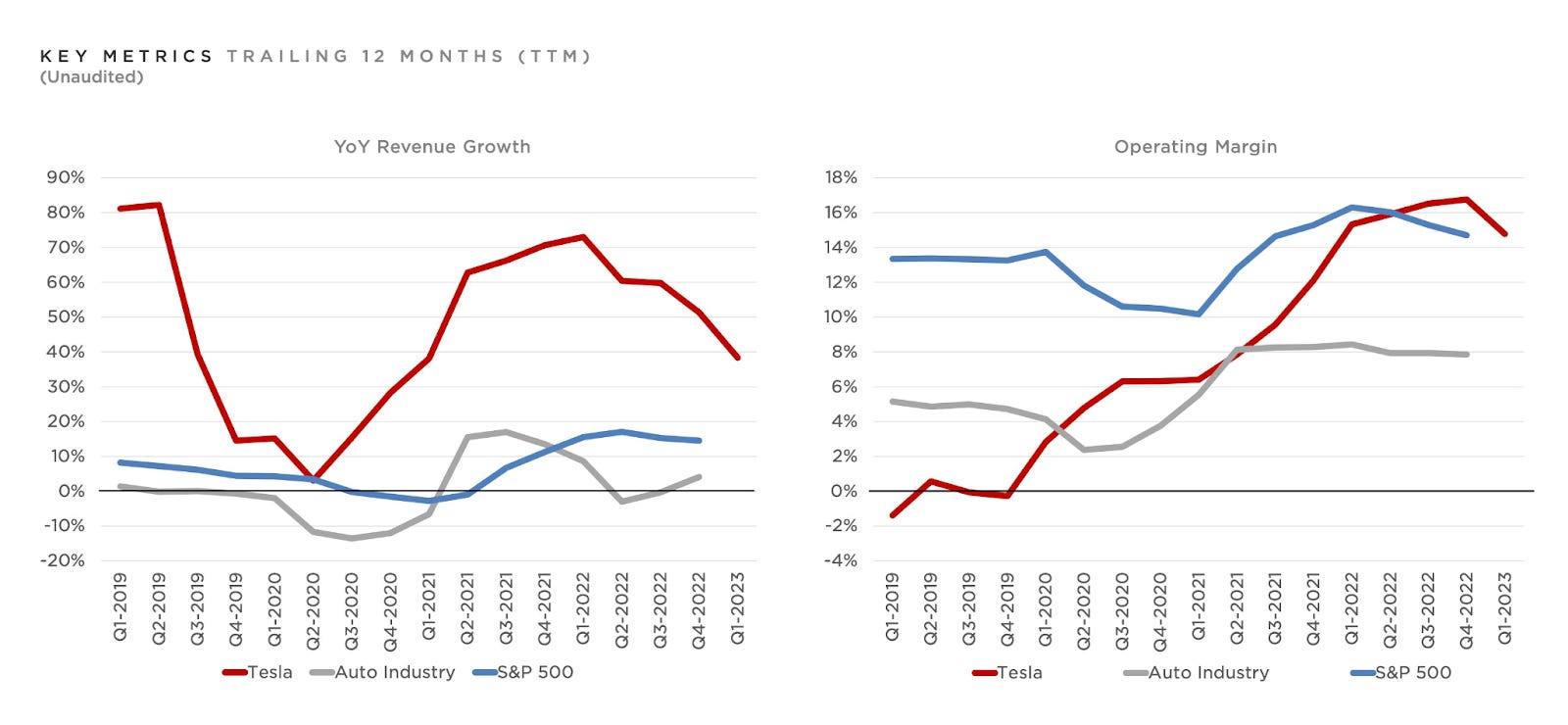

Tesla Slashing Prices

And while we reduced prices considerably in early Q1, it's worth noting that our operating margin remains among the best in the industry…we expect our vehicles, over time, will be able to generate significant profit through autonomy. So we do believe we're like laying the groundwork here, and that it's better to ship a large number of cars at a lower margin, and subsequently, harvest that margin in the future as we perfect autonomy. This is an extremely important point." - Tesla CEO Elon Musk

"Price wars are breaking out everywhere. Who's going to blink for growth? - Ford CEO Jim Farley

And one more thing, Tesla and SpaceX had some big moves. They're making some big moves last week. Elon Musk's the chief tweet, of course,he's doing a lot of things. So of course something to do with Twitter. And of course the issue do with blue ticks and all. But beyond that one, Tesla slashing prices to compete in the market. I think are they finally becoming a car company which has to compete with other brands? And then secondly, of course, SpaceX going out into outer space and all

[00:09:40] Scott: The reason that Elon is saying that they're cutting prices at Tesla would be terrifying to me if I'm another car company that believes him. Because what he's saying is basically, we're gonna make all of our margin on autonomous driving and we're gonna have fully autonomous driving this year. Which obviously Elon pushes timelines and is notorious for not meeting timelines. But if they really do have full self-driving cars this year or anything approximating that, and their strategy is to take the rest of the car and make it a commodity and then make margin on self-driving, they really will disrupt. the automobile industry potentially in a way that the traditional makers won't be able to keep up. And so it is a quite a shot across the bow that maybe people aren't paying full attention to right now despite the fact that everybody pays attention to Elon.

[00:10:30] Mokaya: The funny thing is two days later, they actually did raises prices on some of the goods. So it's a bit, it could be something like it's Elon’s way, maybe he's just shooting a bit and then seeing what happens and then, shifting around a bit until he finds a proper strategy, which he wants to fit in at the end. But it's something interesting because the Ford CEO reacted very sharply and said someone has to blink at the end of the day. So if they're slashing prices, we need to slash prices as well. And Tesla did slash prices in Q1 and it did not impact their profit margin. So I think that may make them bolder to actually make bigger moves in terms of share prices.

Big Week Ahead

But it's a big week in tech earnings.

[00:11:09] Scott: It's a big week of earnings across the board So let's keep an eye on all the companies that are reporting and see what's going on in the economy.

[00:11:18] Mokaya: Definitely 178 S&P 500 companies are actually reporting. So it's a big week. We have to be flipping through a lot of earning transcripts to give you the best quotes. And I think the best place to be is at The Transcript because we digest these things for you and release them every week. So don't miss next week's edition of our newsletter and of course, keep sharing our newsletter because we are reader-supported and we really love and appreciate your being a subscriber to us. So I see you again next week for another edition of The Transcript. Bye from us.

Share this post