In this episode, we discuss the rapid fall of SVB, the subsequent failure of two other banks, and the possibility of contagion.

The episode is based on yesterday's newsletter which is available on Substack.

A transcript of this podcast, with relevant images and quotes, is available for all subscribers after the show notes below. Our podcast is available on Apple Podcasts, Spotify, Google Podcasts, YouTube, and Amazon Music.

Show Notes

00:00:00 Introduction

00:00:07 The Rapid Fall of SVB

00:02:14 The 3 Banks That Failed

00:05:12 Contagion Effects?

00:09:15 Goliath is Winning

00:12:2 Conclusion

Introduction

[00:00:00] Scott: Welcome everyone to a new episode of The Transcript podcast. You've got Mace Scott Krisiloff, I'm editor of The Transcript, along with Erick Mokaya, who's our lead author.

The Rapid Fall of SVB

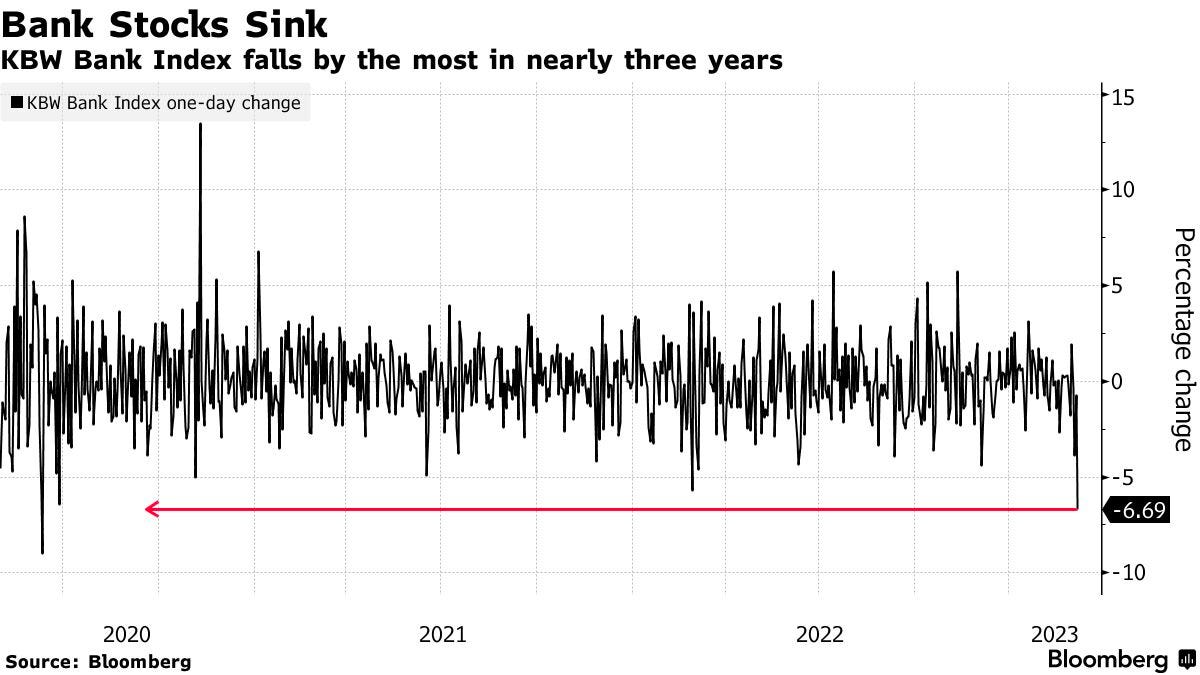

This was one of the stranger issues of the newsletter that we've sent out because I think up until Friday of last week, we really had one newsletter that was written, and then based on Friday and even based on Sunday as I was editing, the message of the newsletter was changing rapidly. Early in the week, it was still about chairman Powell's testimony to Congress and talking about persistent inflation and strong labor markets and what the Fed would do relative to that. And then obviously everyone knows Silicon Valley Bank collapsed in a bank run. Basically from Wednesday evening to Friday morning, it was like about 36 hours and the bank was gone which was a crazy thing to see especially for someone who started his career as a bank analyst in small and mid-cap banks and knows what a respected institution Silicon Valley Bank was. This is something that's very crazy to watch. In some ways was more surprising than things that happened in the financial crisis with the speed with which it happened but in other ways, it's just reminiscent of some of those things that we lived through not too long ago, 15 years ago now. Erick, any thoughts?

[00:01:12] Mokaya: So much to talk about. First of all, this is actually my kind of first real experience with bank runs. I think in the 2008 crisis I was pretty young. I was in my first year at the university, so I hadn't really truly experienced what it was to experience a bank run. I read about it, but it wasn't like practically seeing it happen. So this one was different. It happened on social media. Twitter was not there in 2008. This time it was there. A lot of information was flowing around Twitter. This is the 16th largest bank in the US going from being number 16 to zero. And then this is the second biggest bank to fall since the financial crisis. That's a mild way to put it, but it's pretty huge whatever happened this week. But again, digging into it, what really went wrong with this bank because from the last couple of years, it seems like it's been doing well for many years. It's been here since 1983. So they must have been doing something right for those 40 years to survive that long through the different crises through 2000 and now the 2008 crisis, and now finally actually being wrecked post the pandemic.

The 3 Banks That Failed

[00:02:14] Scott: Yeah. I think at the highest level, just as Silicon Valley Bank is an institution, again, as a bank analyst starting in 2008 and throughout this 15 years as I've been watching public markets, Silicon Valley Bank is viewed as one of the top banking institutions in the country, like one of the great growth banks in the country. And the other two that I would put in that list as well is Signature Bank New York, which is now also shut down and First Republic, which is now under fire as well. These three growth banks which if you look at their stock performance relative to the KBW Regional Bank Index, everything up until last week, these banks had just trounced that index.

[00:02:54] Mokaya: If I may ask, what do you mean by they are growth banks? What's the essence of them? What have they performed? A lot of people know the big banks, the JP Morgans, the Goldman Sachs, and those are the ones which are pretty much involved in the 2008 crisis. But now you have these banks, which are smaller banks, First Republic, Silicon Valley Bank, what makes them distinct from the rest and why is it that there is a bit of a crisis in these three banks specifically?

[00:03:18] Scott: Silicon Valley Bank and First Republic I know really well. Signature Bank less well, and the quality of their client base is really the thing that differentiated them from the rest of the banking arena. But I think this is missing the point as to your question of what happened, which I think what happened is really a very different thing than 2008 as well in that this is not credit driven, this is duration driven. Where in 2008 we were talking about loans going down. In this cycle, what we're seeing is really just mark-to-market losses and long-term government-backed securities. So it's not a question of whether these are money good, it's just a question of whether they're matched duration to the deposit base which is a totally different issue here.

[00:04:01] Mokaya: So if I may add, then I think the issue from my reading at least of the bank, and since I've been examining it, at least in the past week or so, I think it's what happened is that they grew very fast in the past two, three years. But then what happened is the rate hike, and I think the rate hike, there's a saying in the market that the Fed hikes until something breaks. We've been seeing a bit of signs that some parts of the financial systems are under stress, and then the past week or so, suddenly something broke, and that was Silicon Valley Bank because customers wanted their deposits back, but now they've invested in some long-term assets, which they can't sell very quickly to be able to fulfill the demands. And then everyone tells everyone, hey, this duration mismatch is a big issue. Pull out your money. And then in a week they had 40 billion worth of deposits that were taken out. And then that at the end caused the bank run. But from where you're sitting now, what's the perspective of the people around you in terms of how quickly this happened? And do you think this changes also the perspective of the Fed more moving away from fighting inflation now to containing a system-wide kind of contagion that may be happening because of Silicon Valley Bank?

Contagion Effects?

[00:05:12] Scott: Well, it could, It could, that is definitely the question that we'll be watching and assessing in the next several weeks. Obviously the Fed meets next week to set interest rate policy and there's already articles in the Wall Street Journal talking about them maybe not raising rates as quickly or leaving rates unchanged next week as they assess the impact of this stuff. But yeah, the way that changing narrative often happens is that there's some big event like we just went through with Covid that changes is the frame of reference that everybody is analyzing the world through. And the Silicon Valley Bank collapse last week feels like one of those, maybe not as large as Covid, but it certainly feels like a firing gun on something changing for the narratives here. And that was again, part of the reason why it was tough to write this week's issue is because we saw some big change right at the end of the week and it's unclear how things were going to evolve based on that. But whether or not this is a longer-term thing that changed or a shorter-term thing, I've been thinking, is this the sign that we're actually finally at the start of the recession? Is this the firing gun for the recession? Even if it is, a lot of times, that just means that it's time for the bull market to start when a recession starts, sometimes bull markets just start because the Fed comes in and starts easing monetary conditions as well. But the Fed is really walking this odd barbelled economy where you've got potentially financial risk building among regional banks and potentially spreading, and then you've also got their mandate of inflation pushing down on them. I don't know how they're going to necessarily square those two here. Probably bias towards not letting financial contagion happen. So that may be the winning factor here or the big change.

[00:07:00] Mokaya: I think that's a bigger risk because it has a contagion effect, not just within the US financial system, but it's global. This morning, we are recording this on a Monday. So this morning the UK financial system had to deal with the same issues the US was dealing with. There was a bit of a bank run that was almost going to happen in the UK branch of the Silicon Valley Bank, and in the end HSBC had to step in, buy it for one pound and then take over its operations and allow it to continue to flow smoothly. So what you can sense is that once something like this happens, it's a regional bank in the US that this is happening at, then its fall raises issues about the entire financial system because everyone is asking, is my bank safe? And someone else is in a different part of the world in Africa, he's also asking the same question, what does that mean for me, where I am?

[00:07:47] Scott: Yeah. This is the fundamental thing that's different about this time than 2008 that I don't know that markets are fully appreciating quite yet is this actually just flies in the face of the regulatory regime that was established really prior to 2008, but especially reinforced post 2008, which is that you are supposed to hold capital against risky assets and government backed securities are not risky assets, so you can have high tier one leverage ratios, which are adjusted for zero risk weighting to government securities and you can go as far out the duration curve as you want on that. And then on the other side, remember in 2008, the problem was viewed as not having enough of a core deposit base funding basis for investment banks. That's how the investment banks failed because they were short-term funded through commercial paper markets, not through deposit markets. And that's why they were deemed to be unsafe. So in this case, you're a company that basically only had held zero risk rated assets and was core deposit funded and still was basically caught up in this very fast-moving world of the internet that we have now. And it may just be the case that fundamentally, high-leverage banking models are not sustainable in a world where you can pull all of your deposits overnight, 200 billion worth of deposits just out the door. The regulatory regime is not prepared for this sort of dynamic.

Goliath is Winning

[00:09:15] Mokaya: Significantly think of it. Somebody was able to pull out 40 billion from a bank last week over one or two days last week, and managed to actually run down a bank or cause a bank run at the bank. That tells you a lot about how this kind of modern digital kind of banking has also influenced a lot. So in the old days, you had to actually go to the bank to make a bank run. Now you can just switch on the phone and switch very quickly and send money, wherever it is that you wanted to send to. But then I think one of the other things that I've also noted now, one of the banks that was up on Friday when everyone notice there was JPMorgan. Seems like Dimon the too big to fail banks are actually going to get even bigger because they're going to get more people wanting to put their money in banks that are actually safe at the end of the day. So I think another thing that people are paying attention to a lot is the level of uninsured deposit that you have. Silicon Valley Bank had almost close to 90% of its deposits uninsured. That was not an issue back then, but now I think everyone is paying attention to it. Is my money insured? Is it not insured? And some of the banks are actually performing poorly in the market today, have to do with having very high uninsured level of deposits. I think there's a lot of mistrust suddenly in the market, which wasn't there before.

[00:10:33] Scott: Yeah, again, the deposits are insured in a way. All deposits especially in this case of Silicon Valley Bank. The assets that were backing deposits were government guaranteed securities. What was the problem was they had duration risk to them, right? Because as interest rates change the current market value of those changes, but the fundamental cash flows backing those securities are guaranteed by the US government already. So I guess what the US government would need to do and really shouldn't have that hard time of doing through the Fed, is just guarantee the duration risk against those assets to the extent that they want to guarantee all deposits across the banking system. If I'm looking for somebody to lend to you long term as a government, I guess that's what you need to do.

[00:11:23] Mokaya: Which way from here now, because there's a bit of stress in some of the other financial institutions in the system except the big banks. There's going to come regulations once more because Silicon Valley was on the verge of becoming one of the big banks. It was moving from regional to being one of the big banks. It hadn't been done on liquidity tests on it for a long time. Somehow theY escaped kind of federal regulations and all. So I bet there will be regulations on this kind of banks going forward again. So the response is most likely going to be more regulations for the banks. And more requirements maybe to keep insured deposits and all. What do you see from your end in terms of going forward on the implications of this?

[00:12:08] Scott: I don't know. It'll be interesting to see. It depends how crazy this little mini-banking crisis that we're seeing right now is. I don't think there's necessarily political will to change any regulations based on anything that's happened so far. But if it gets a lot worse, there probably will be.

Conclusion

[00:12:26] Mokaya: Alright. There's a lot to speak about, we probably should have a Twitter space this week or next week on this, depending on how things move. Anything else that may have caught your eye in the market this week?

[00:12:36] Scott: Hard to focus on much of anything besides Silicon Valley Bank and the regional banking space.

[00:12:42] Mokaya: Alright. To keep track of what's happening in the market, especially key quotes from earning calls and from key leaders, just follow us on Twitter. We're very active there. Keep up with us on Twitter @thetranscript_ and of course, keep it here for another podcast next week as we try to discuss and unravel what happens about this Silicon Valley Bank collapse. Bye for this week.